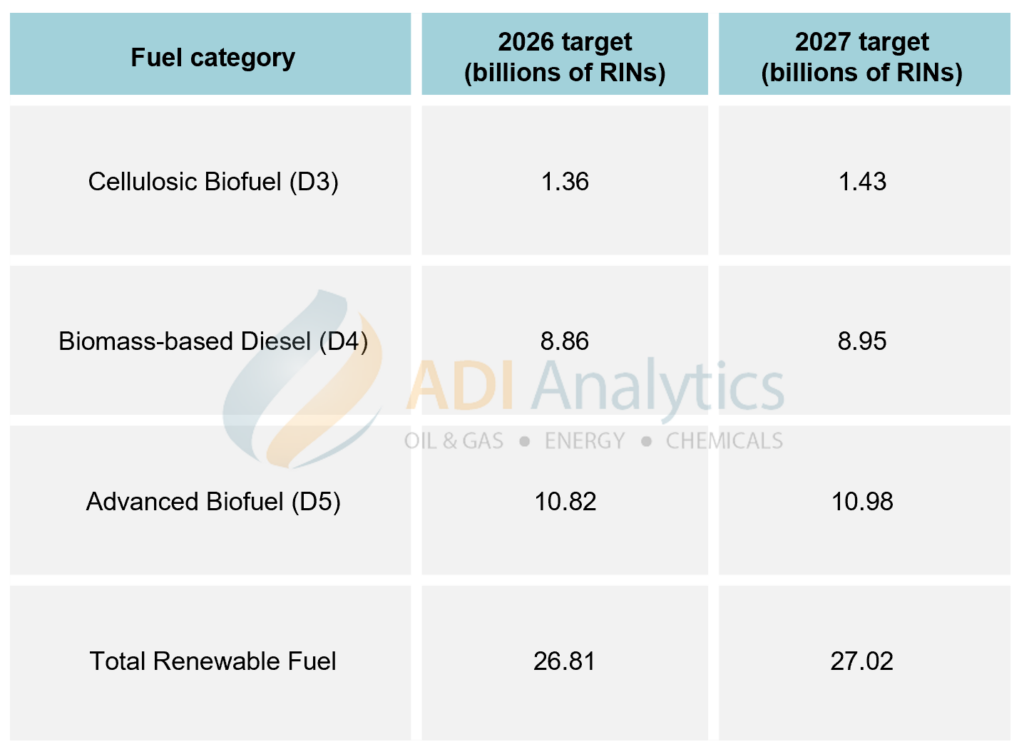

The U.S. Environmental Protection Agency (EPA) recently finalized the Renewable Volume Obligations (RVO) for 2026 and 2027, establishing the highest blending mandates in the history of the Renewable Fuel Standard (RFS) program (see Exhibit 1). The RFS requires oil refiners (“obligated parties”) to blend specific volumes of renewable fuels into the U.S. transportation fuel supply or purchase compliance credits called Renewable Identification Numbers (RINs). The new rule sets total requirements at 26.81 billion RINs for 2026 and 27.02 billion RINs for 2027, creating a structurally tight market for these credits by simultaneously increasing demand and limiting supply options.

Exhibit 1. U.S. EPA’s renewable volume obligations for 2026 and 2027.

Demand is being pushed higher because the EPA is reallocating approximately 70% of the fuel volumes previously waived under Small Refinery Exemptions (SREs) from 2023–2025 back into future mandates. This move adds an estimated 2.89 billion RINs of demand back into the system. To further tighten the market, the EPA has removed renewable electricity (eRINs) as a compliance option and delayed penalties (expected at a 50% reduction in value) on cheaper foreign imports until 2028. For refiners, this means they must rely almost exclusively on domestic liquid biofuels, such as renewable diesel and ethanol, to meet these aggressive new federal targets. The result is a system where incremental compliant supply carries disproportionate value.

How can biofuel players navigate this market? Based on our work in biofuels, ADI sees the following strategic opportunities:

Carbon intensity reduction as a cash flow driver

In a tight RIN market, lower-carbon fuels capture higher combined value from RINs, LCFS programs, and the 45Z clean fuel production credit. Even small carbon intensity (CI) reductions can materially increase revenue per gallon. Ethanol producers with sufficient scale can invest in technical upgrades that lower facility carbon intensity by 25 to 30 points. These adjustments include fermentation carbon capture and storage (CCS), mechanical vapor recompression (MVR), and membrane dehydration. In ADI’s work on large-scale ethanol assets, these types of upgrades have consistently shifted project economics by increasing the value of each compliant gallon. Such engineering updates can unlock over $70 million in incremental annual revenue for a 100 MMgy plant.

Plant ownership gives existing facilities an edge in supplying aviation fuel

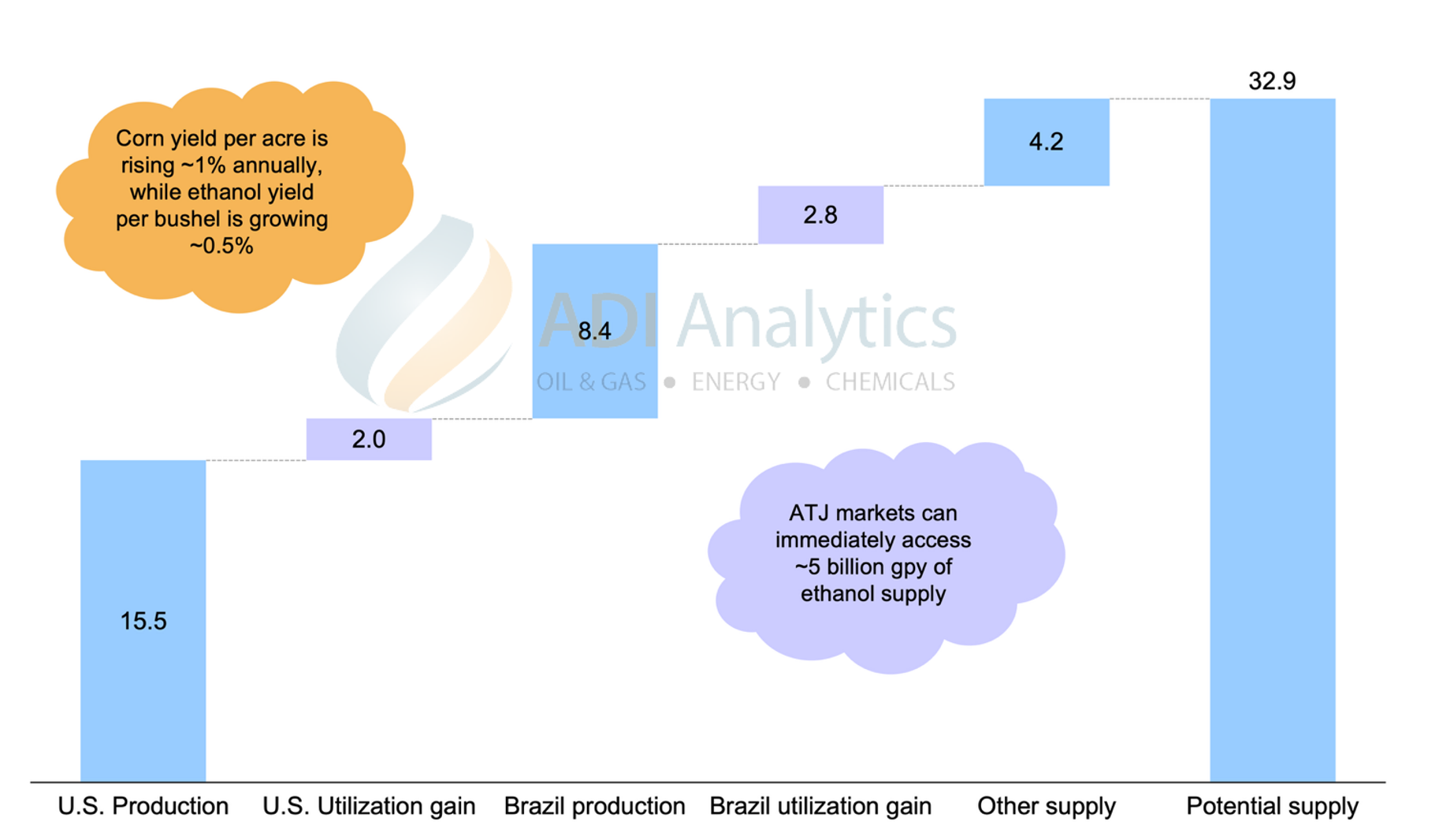

Biomass-based diesel targets are now set at historic highs, and when including refinery reallocations, the pressure on supply will be intense. Renewable diesel and biodiesel utilization will likely need to exceed ~90% over the next two years to meet demand, tightening feedstock availability. This dynamic pushes producers to explore alcohol-to-jet (ATJ) pathways more seriously. In this supply-constrained system, existing ethanol facilities have hard-to-replicate advantages—permits, grid interconnections, rail access, and storage utilities—that reduce capital and execution risk for SAF expansion. Further, existing facilities can be revamped to increase ethanol production as we show in Exhibit 2. ADI’s assessments of SAF pathways and markets have repeatedly shown that these existing assets function as advantaged starting points for SAF buildouts.

Exhibit 2. Global ethanol production growth potential in 2023 with minimal investments.

Broadening co-product lines diversifies revenue streams

Higher effective mandates increase the value of total plant output, but co-product upgrades primarily help stabilize earnings rather than expand RIN supply.

Upgrading secondary streams protects a producer’s earnings when ethanol margins fluctuate. Plants can route fermentation CO₂ to permanent underground storage, upgrade distillers grains (DDGS) into specialty feeds, and maximize corn oil extraction. In ADI’s work on plant monetization strategies, these levers consistently improve total plant economics without requiring incremental feedstock.

Feedstock tracking prevents future regulatory compliance cliffs

In a tight market, access to compliant feedstocks enables participation in high-value RIN pools. The EPA’s decision to delay import RIN penalties until 2028 creates a defined window for producers to reposition supply chains.

Source verification determines lifecycle carbon scores and long-term market access. Securing multi-year contracts for climate-smart and regenerative corn ensures eligibility for premium markets and reduces future compliance risk as standards tighten. ADI’s feedstock risk studies indicate that early moves on traceability and contracting materially improve positioning ahead of the 2028 transition.

Advanced processing methods lower baseline manufacturing costs

Tight markets support margins, but cost position determines resilience when conditions ease. High capital costs for new plants increase the value of upgrading existing facilities. Producers can achieve deep efficiency gains within their current operating footprint.

ADI process benchmarking indicates that shifting from batch to continuous or semi-continuous fermentation, combined with advanced heat recovery, can reduce operating costs by 20% to 50%. These retrofits lower the minimum RIN price required for profitability, preserving competitiveness across cycles.

Capital allocation implications

The 2026–2027 RVO framework establishes that volume growth alone is insufficient to capture value. Companies must direct capital toward turning single-product processing facilities into multi-product chemical and fuel platforms. Asset valuation will increasingly depend on how fast a company deploys carbon-reduction technologies, secures verified domestic feedstocks, and adapts its operations to serve emerging aviation and industrial markets.

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.