We recently attended the 2026 American Bioeconomy Leadership Conference (ABLC) in Washington, D.C., just as U.S. policymakers signaled a renewed willingness to use biofuels as a tool for fuel market stability. The EPA’s announcement allowing a temporary nationwide waiver for E15 gasoline sales underscores how energy security, agricultural policy, and domestic fuel supply resilience are converging in the current policy environment. Against this backdrop, conference discussions reinforced a central theme: the bioeconomy is entering a more disciplined phase, defined less by technological ambition and more by economics, policy execution, and scalable deployment. The following ten insights summarize the structural forces shaping its trajectory over the next decade.

1. Unit economics outrank technological novelty

Complex pathways such as cellulosic ethanol failed to scale because they could not achieve cost parity with incumbent fuels. By contrast, corn ethanol, biodiesel, renewable diesel, and renewable natural gas reached billion-gallon scale by demonstrating commercial viability and competitive production costs (see Exhibit 1). Future success will depend on targeting markets with proven, bankable unit economics rather than unproven technological elegance.

Exhibit 1. Renewable fuels that have achieved billion gallon scales in the U.S. (Source: Iogen)

2. Carbon Intensity (CI) is the primary financial lever

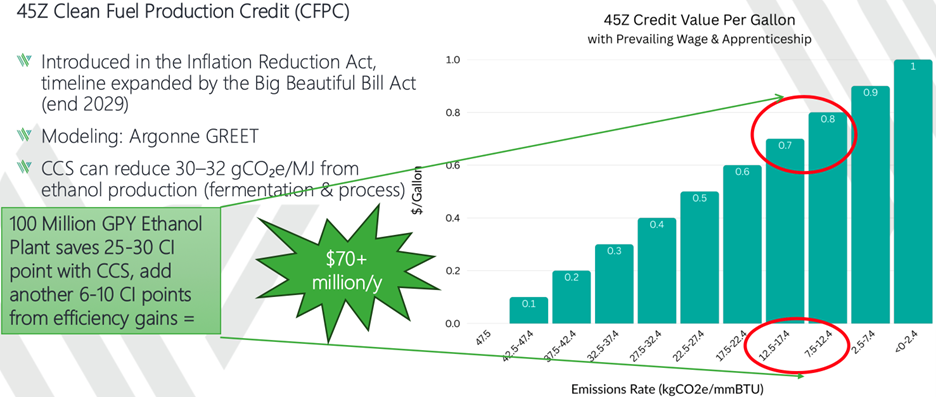

Profitability is now directly linked to reducing lifecycle CI scores to maximize regulatory incentive value, particularly under the 45Z production tax credit. Adding carbon capture and storage to a 100‑million‑gallon‑per‑year ethanol plant can lower CI by 25 to 32 points, unlocking more than $70 million in incremental annual revenue (see Exhibit 2). Operational improvements now translate directly into margin expansion.

Exhibit 2. Economic value of pairing CCS with ethanol production in the U.S. (Source: Whitefox Technologies)

3. Sustainable Aviation Fuel faces structural cost ceilings

Scaling SAF requires permanent mandates to bridge its cost disadvantage versus conventional jet fuel. SAF represents roughly 1% of global biofuel supply today. In early 2026, conventional jet fuel averaged $6.34 per gallon in the U.S., while SAF traded at roughly $8.43 per gallon—a premium that limits voluntary adoption without policy support.

4. Feedstock diversification requires data standardization

SAF demand will soon outstrip the supply of easily processed lipid feedstocks such as used cooking oil and animal fats. The industry must shift toward heterogeneous inputs including solid waste, cellulosic biomass, and biomethane. Managing the physical and chemical variability of these feedstocks requires robust data curation, with thousands of compositional variables tracked to optimize conversion performance.

5. Infrastructure repurposing circumvents deployment delays

In many OECD countries, permitting timelines match or exceed construction timelines. Developers are therefore prioritizing retrofits of existing refineries and co‑processing biogenic feedstocks within established infrastructure. This approach reduces capital intensity, lowers regulatory risk, and significantly accelerates deployment versus greenfield builds.

6. Decentralized production unlocks stranded assets

Centralized facilities face high logistics costs when sourcing dispersed agricultural feedstocks. Modular, standardized production units located at dairy farms, wastewater treatment plants, and forestry sites enable on‑site conversion of biomass and biogas. This model eliminates the cost of transporting low‑energy‑density materials and improves overall system economics.

7. High‑value biochemicals subsidize fuel scale‑up

Single‑product fuel models are exposed to policy risk and margin compression. Producers are increasingly adopting multi‑product platforms that can shift output across fuels, specialty chemicals, and performance materials. Upgrading intermediates into higher‑margin products provides demand stability and commercial ballast during early‑stage scale‑up.

8. Geopolitics accelerate localized supply chains

Energy security concerns and import‑substitution priorities are driving capital toward domestic bio‑manufacturing. Governments increasingly view biomanufacturing capacity as a strategic asset, not just a decarbonization tool. National mandates create immediate local markets and underpin investment in resilient domestic production infrastructure.

9. Policy implementation bottlenecks capital deployment

While headline policy support exists, administrative delays and uncertainty around credit qualification continue to stall project development. Inconsistent frameworks and unclear emissions accounting rules limit capital deployment. Durable policy design and objective, financeable rules remain prerequisites for first‑of‑a‑kind plants to reach final investment decisions.

10. E‑fuels face severe near‑term cost barriers

E‑fuels produced from captured CO₂ and green hydrogen remain uneconomic at scale, with unsubsidized e‑SAF costs exceeding $20 per gallon. Near‑term deployment will favor pragmatic biomass conversion pathways and hydrogen co‑processing rather than capital‑intensive carbon‑to‑fuel technologies.

– Uday Turaga

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.