A sharp debate is currently playing out across the energy and tech sectors. On one side, hyperscalers are deploying unprecedented capital to vertically integrate power generation and bypass multi-year interconnection queues—exemplified by Google’s recent multi-billion-dollar acquisition of energy developer Intersect Power. On the other side, experts like Jigar Shah warn that tech companies cannot simply build their way out of local constraints, noting that communities have already stalled or blocked more than $156 billion in data center developments.

This tension confirms what we are seeing across the market: the data center industry has officially shifted from a phase of speculative planning to an aggressive, high-stakes infrastructure execution phase. Demand is no longer the variable; the bottleneck is now the physical reality of grid capacity, local politics, and equipment supply chains.

Based on ADI’s advisory work with hyperscalers, developers, utilities, investors, and industrials across the data center value chain throughout 2026 so far, we have analyzed the market to identify five key trends shaping the infrastructure landscape:

- Mega-campuses face intense local bottlenecks

The development pipeline is increasingly dominated by multi-gigawatt “AI factories” designed to address the speed-to-power challenge. Notable examples include Meta’s Hyperion campus (projected to scale from 1.5 GW in 2027 to 5.0 GW over time) and the Oracle/OpenAI “Stargate” project targeting up to 10.0 GW.

However, this rapid expansion is running directly into tightening regulatory and community resistance. In the first quarter of 2026, Maine enacted a moratorium on data centers exceeding 20 MW, while Google withdrew a 468-acre project in Indiana following local opposition. These dynamics highlight a growing clash between hyperscale ambitions and regional constraints. To map these shifting dynamics, our team continuously tracks real-time project timelines, delays, and capacities through ADI’s U.S. data center projects database. - Developers pivot to agile micro-inference clusters

Regional bottlenecks are driving a complementary countertrend: the rise of smaller, distributed infrastructure optimized for AI inference rather than massive model training. While model training requires highly centralized power capacity, inference workloads can sit much closer to end users.

Industry leaders like NVIDIA and EPRI are exploring facilities in the 5 MW range, while developers increasingly target sub-100 MW projects to stay below “large load” regulatory thresholds. This shift allows for faster deployment timelines, greater flexibility, and significantly less local resistance. - Behind-the-meter power strategies evolve with utility sharing

To bypass grid interconnection queues that now stretch beyond five years in major regions, operators are turning to “Bring Your Own Power” (BYOP) structures. Amazon has secured 960 MW directly from the Susquehanna nuclear plant, and Meta has signed agreements for up to 6.6 GW of nuclear capacity through 2035.

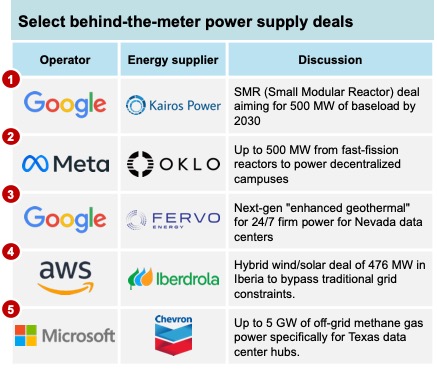

Crucially, hyperscalers are not fully disconnecting from the grid. Instead, they are collaborating with utilities to act as dispatchable load stabilizers. For example, NiSource’s pooling agreement with Google and Amazon in Indiana is projected to deliver $1.25 billion in system-wide savings while protecting retail ratepayers from rising infrastructure costs. Exhibit 1 below summarizes select behind-the-meter power supply deals signed recently.

Exhibit 1. Select behind-the-meter power supply deals.

- Liquid cooling adoption accelerates rapidly

As next-generation GPUs breach the 1,000W-per-chip threshold, traditional air cooling can no longer keep up. Liquid cooling is quickly becoming the baseline standard, with global penetration projected to jump from 3% in 2023 to more than 40% by 2028.

This quick transition is creating high-margin opportunities for providers of advanced cooling fluids and thermal management systems, specifically direct-to-chip and immersion technologies. However, supply chain readiness remains a critical question; as detailed in our analysis on how cooling fluids are becoming a constraint in AI data centers, the chemistry and scaling of these specialized fluids represent a major operational roadblock for next-gen deployments. - Equipment supply bottlenecks dictate project timelines

Supply chain constraints are now the primary limiting factor for near-term commissioning dates. Specialized electrical equipment manufacturers are facing unprecedented backlogs, as ADI has previously noted, now highlighted by Eaton’s 240% surge in data center orders in Q1 2026.

Lead times for heavy equipment, such as industrial gas turbines, have stretched out to 250 weeks. Proactive, programmatic procurement strategies are no longer a luxury—they are a prerequisite for viable project execution.

The organizations that succeed in this environment will be those that stop viewing AI data centers as a pure software story and start treating them as complex physical industrial systems. Balancing local ratepayer impact, securing long-lead equipment, and optimizing power sharing will separate the projects that get built from those that remain on paper.

Contact ADI Analytics to explore how our 2026 market intelligence and data tools can support your infrastructure, power procurement, and supply chain strategy.

– Panuswee Dwivedi and Uday Turaga

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.