The U.S. data center market is growing rapidly as rising computational demand from artificial intelligence (AI), cloud computing, and high-performance computing continues to drive an unprecedented wave of infrastructure development. In 2025, U.S. operational data center capacity is estimated to have reached ~40 gigawatts (GW) and is expected to grow at roughly 30% annually through 2030. ADI projects that the U.S. data center market could add ~115 GW of new capacity by 2030, representing a significant expansion from current installed levels.

Some of the notable hyperscale data center projects expected to come online over the next several years include:

- PORTS Tech Campus, Ohio — 10.0 GW, expected 2028–2029

- GW Ranch Data Center, Texas — 7.7 GW, expected 2027

- New Era LEA AI Data Center, New Mexico — 7.0 GW, expected 2028

- Monarch Compute Campus (Phase 2), Virginia — 6.0 GW, expected 2031

- Meta Hyperion AI Data Center, Louisiana — 5.0 GW, expected 2030

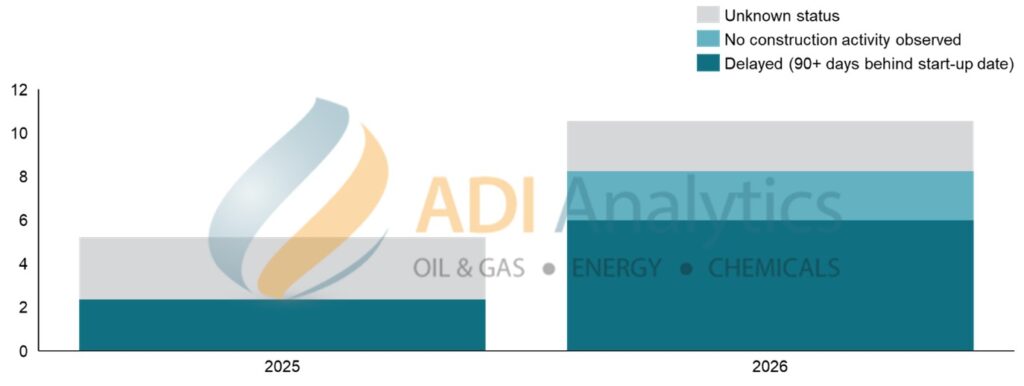

Despite strong demand growth anticipated, planned data center projects are increasingly facing constraints that could slow development, including limited power availability and grid interconnection bottlenecks, cooling limitations, long lead times for critical equipment, land and permitting challenges, and labor shortages. As shown in Exhibit 1, ~2.5 GW of data center capacity experienced delays in 2025, while an additional ~8.5 GW of planned capacity is expected to face delays, as several projects showing limited or no updates on construction progress.

Exhibit 1: U.S. data center development status (GW). (Source: JLL, ADI)

With a growing number of hyperscale data centers being developed to support AI workloads, these factors are becoming increasingly important in determining where and how quickly projects move forward. ADI’s U.S. data center projects database and services support strategic decision-making for data center developers and operators, power suppliers, equipment providers, investors, and other stakeholders across the broader data center ecosystem, including siting and power strategy, grid and infrastructure planning, supply chain risk, and investment opportunity assessments. Designed to provide timely market intelligence on the evolving U.S. data center market, the database includes comprehensive information on project developers, locations, power capacity, land footprint, development status, and expected start-up timelines.

Based on the database, ADI identified five key observations shaping the U.S. data center market:

The rest of this article is available to all ADI Plus subscribers. ADI’s U.S. data center projects database is available exclusively for ADI Plus Enterprise subscribers.

Log in or subscribe to unlock ADI Plus content >>

Have questions? We're happy to help.

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.