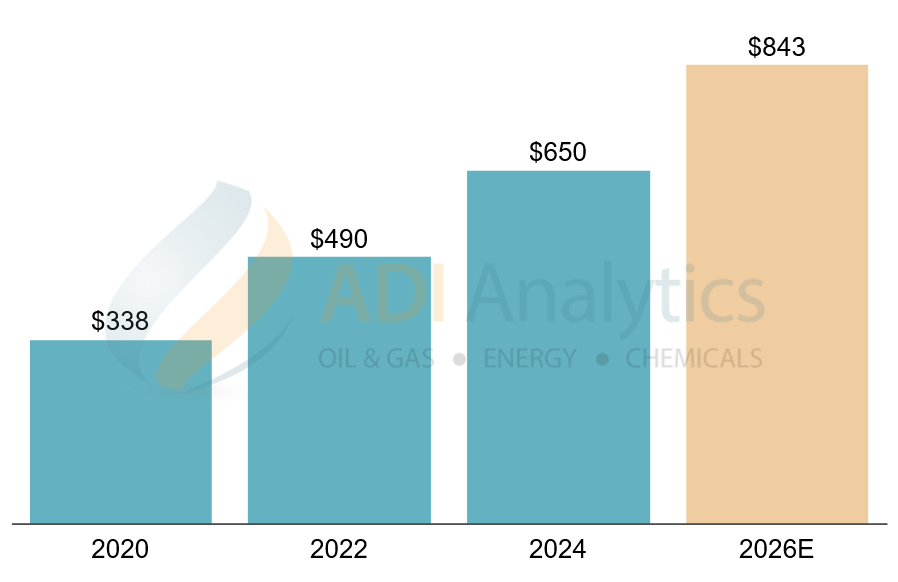

U.S. utilities are entering the largest capital deployment cycle in their history, with total spending projected to reach roughly $1.4 trillion through 2030 and annual capex growing at double-digit rates.

The single biggest driver behind this surge is the rapid growth in AI and data centers. Hyperscale facilities are significantly increasing load demand, often on accelerated timelines, forcing utilities to expand generation, transmission, and interconnection capacity simultaneously. At the same time, other factors including industrial reshoring, electrification, grid hardening, and policy support are also contributing to rising demand and infrastructure needs. Together, these drivers are pushing utility capital programs to unprecedented scale.

Exhibit 1: Aggregate 5-year capex plan of U.S. utilities (Billion USD). (Source: Company investor presentations, ADI Analytics)

Execution is falling behind

While spending is accelerating, execution is not keeping pace. Delays and cost overruns are widespread across the project landscape.

In early 2026, approximately 60% of planned solar projects and 50% of battery storage projects experienced delays, with a large share of new capacity expected to miss original in-service dates. At a broader level, only a small percentage of megaprojects are delivered both on schedule and on budget.

Well-known projects illustrate the challenge. The Vogtle nuclear expansion, for example, faced significant cost increases and multi-year delays before reaching completion. Offshore wind developments have also seen similar pressures, with projects such as Coastal Virginia Offshore Wind requiring cost revisions and schedule adjustments during execution.

Headwinds are building

Three factors are showing up consistently across projects.

First, supply chain bottlenecks remain severe. Lead times for key equipment such as transformers and gas turbines now extend several years, while global manufacturing capacity remains concentrated among a small group of suppliers.

Second, workforce shortages are limiting execution capacity. Nearly half of the utility engineering workforce is approaching retirement, and shortages of skilled trades and project leadership are slowing construction activity and increasing costs.

Third, regulatory and permitting timelines continue to extend. Interconnection queues alone can take years to clear, and increased scrutiny around cost recovery is raising the stakes for project performance.

These pressures are compounding. As project pipelines grow, constraints in one area quickly cascade into broader delays.

Reliable delivery defines performance

With capital availability no longer the primary bottleneck, execution has become the differentiator. Utilities that can deliver projects reliably are better positioned to capture growth, maintain regulatory support, and protect returns.

In response, leading utilities are strengthening project governance, adopting more flexible contracting strategies, and investing in tools that improve cost and schedule visibility. However, the gap between leading and average performance remains significant, and many organizations are still adapting to the demands of this cycle.

Learn More

If your organization is preparing to deploy significant capital, we invite you to download the prospectus for ADI’s latest multi-client study on capital project excellence in the utility sector. The study provides a detailed view of the capex landscape and where projects are breaking down, along with benchmarks on cost and schedule performance and practical insights on how leading utilities are improving delivery through governance, contracting, and supply chain strategies.

Subscribers will gain a clear, data-driven roadmap to reduce execution risk and improve project outcomes across the lifecycle. The work will be delivered over an eight-week timeline, with interim findings, workshops, and a final report, followed by ongoing updates.

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.