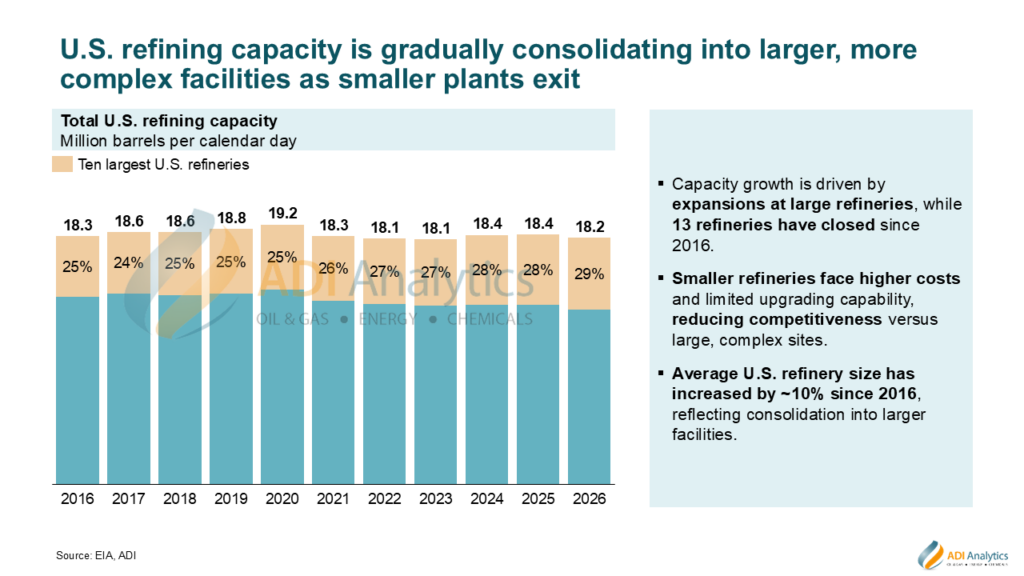

U.S. refining capacity shows limited overall growth, but the structure of the system is shifting. Expansions at large, complex refineries are driving changes on the supply side, while smaller plants face cost and operational constraints that are forcing exits. This is steadily concentrating capacity in fewer, more sophisticated facilities.

Key drivers capacity consolidation:

- Large refineries continue to expand, with brownfield projects and incremental upgrades driving most capacity additions.

- Smaller plants face structural cost pressures, including higher compliance costs and limited upgrading capability.

- Policy and energy transition dynamics are accelerating closures and conversions, particularly in more regulated markets.

- Geographic concentration supports scale, with Gulf Coast complexes benefiting from logistics, integration, and export access.

Geographic concentration supports scale, with Gulf Coast complexes benefiting from logistics, integration, and export access.

This shift is improving efficiency through scale and complexity, but it comes at the cost of reduced system redundancy. As a result, supply becomes more exposed to disruptions at a limited number of critical assets.

For a more detailed, refinery-level view of U.S. capacity, explore ADI’s U.S. refinery database.

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.