Part of ADI Analytics’ ongoing coverage of the implications of the Iran conflict across oil & gas, LNG, refined products, and chemicals.

Oil prices have surged again, driven by the Iran conflict and fears of disruption in the Middle East. These risks matter, and they explain today’s prices. But history and current fundamentals suggest they are unlikely to hold oil at elevated levels through 2026. Several forces point to oil returning to the $60s by the end of this year.

1) The global economy is slowing, and recession risks are rising

The IMF’s April 2026 World Economic Outlook lowered global growth expectations and warned that the Middle East conflict represents a negative shock to the world economy through higher energy prices, tighter financial conditions, and weaker consumer purchasing power. Under adverse scenarios, the IMF sees global growth falling toward 2%, which it describes as close to recession territory.

Oil demand historically weakens sharply in late‑cycle slowdowns. Transportation, petrochemicals, and industrial fuel use tend to soften quickly when growth slows. Prolonged oil prices above $90 would likely worsen this slowdown, accelerating demand destruction rather than sustaining high prices.

2) The oil market entered 2026 already looking oversupplied

Even before the war, global oil balances were pointing to surplus. ADI and other forecasters estimate that global supply exceeds demand by roughly 2–4 million barrels per day (MMbpd) in 2026, driven by non‑OPEC growth from the U.S., Brazil, Guyana, and offshore projects coming online.

This matters because geopolitical shocks lift prices most when markets are already tight. In an oversupplied market, they tend to raise volatility but do not establish a new long‑term price floor.

3) Forward oil prices already assume normalization

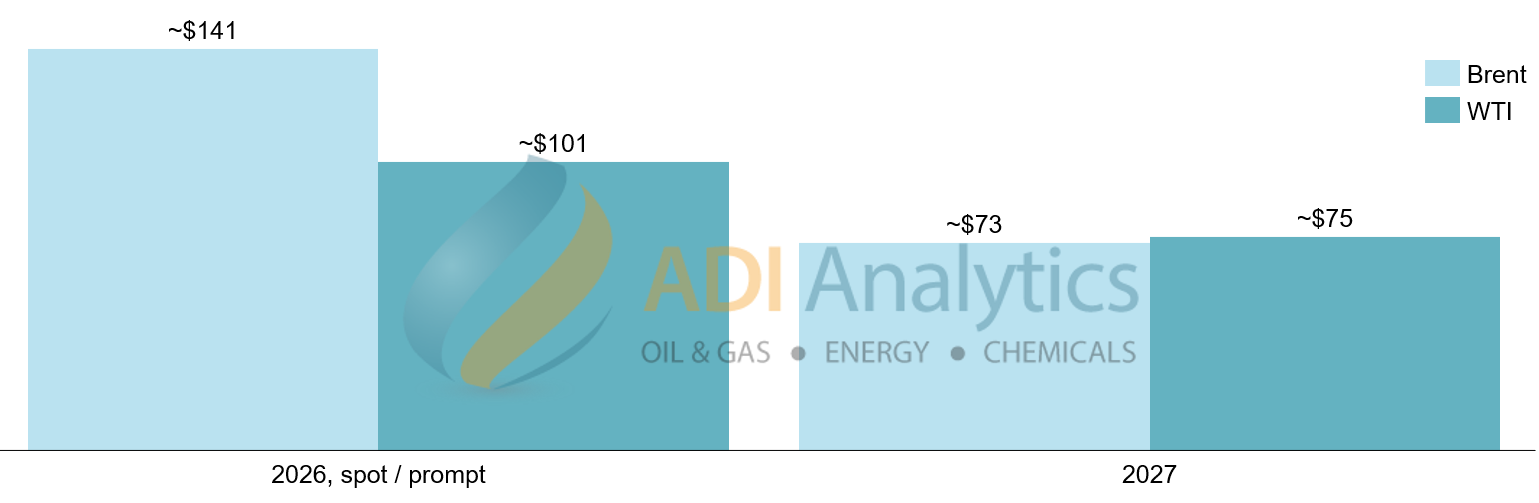

While spot prices reflect near‑term fear, longer‑dated oil prices tell a different story. The futures curve falls sharply beyond the front months, with prices for 2027 trading far below current levels (see Exhibit 1).

Exhibit 1. 2026 spot oil prices vs. 2027 forward trade prices (USD per barrel, $/bbl).

This structure signals that traders expect the current disruption to fade and supplies to rebalance. Markets that believe shortages will persist typically price future barrels higher, not lower.

4) High gasoline prices create political pressure to lower oil prices

Fuel affordability remains a powerful constraint. Higher oil prices feed directly into inflation, consumer sentiment, and election politics. In the U.S. and other large consuming economies, sustained gasoline prices near recent highs are difficult to tolerate, particularly heading into election cycles.

Historically, periods of strong political pressure coincide with efforts to stabilize or de‑escalate geopolitical tensions and encourage supply. These forces rarely support sustained high oil prices for multiple years.

5) Capital discipline limits upside, but still allows supply growth

Oil companies remain cautious on spending, but that does not mean supply stops growing. U.S. production continues to expand modestly through offshore projects and efficiency gains, while OPEC producers retain substantial spare capacity that can return once risks ease.

With demand growth slowing and supply still rising at the margin, the balance increasingly favors lower prices into 2027.

6) Past conflicts show risk premiums fade faster than expected

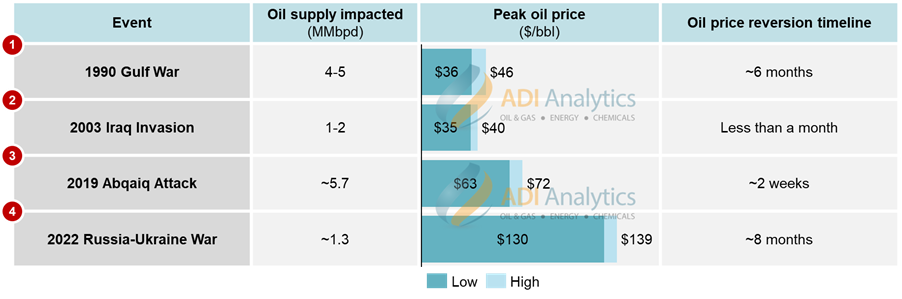

History offers a clear lesson. Oil price spikes linked to geopolitical conflicts—from the Gulf War in 1990 to the Russia-Ukraine invasion in 2022—typically reverse within months once the situation stabilizes (see Exhibit 2). Prices often return to pre‑crisis levels well before the physical and political damage is fully resolved.

Exhibit 2. Oil price reversion timelines after major supply shocks. (Source: ADI)

There is little evidence that the current conflict has permanently removed enough supply to justify elevated prices through 2026.

In summary, geopolitical risks can keep oil volatile in the near term, but slowing growth, an underlying supply surplus, political constraints, and market pricing all point in the same direction. Absent a prolonged physical loss of supply, oil prices are more likely to drift back into the $60s by the end of 2026 than remain near today’s levels.

– Uday Turaga and Edmund Lam

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.