Demand for critical minerals has been accelerating rapidly over the past few years, driven by escalating growth in electric vehicles, renewable energy, defense, and advanced technologies. However, while demand continues to expand, the supply chain remains heavily concentrated in China, which dominates up to 90% of mining, refining, and processing.

This imbalance has amplified geopolitical risks. Export restrictions and policy interventions have created supply volatility and heightened concerns around long-term security. As a result, the industry is shifting from a price- and efficiency-led model to a security-first framework, reshaping investment priorities and global trade flows.

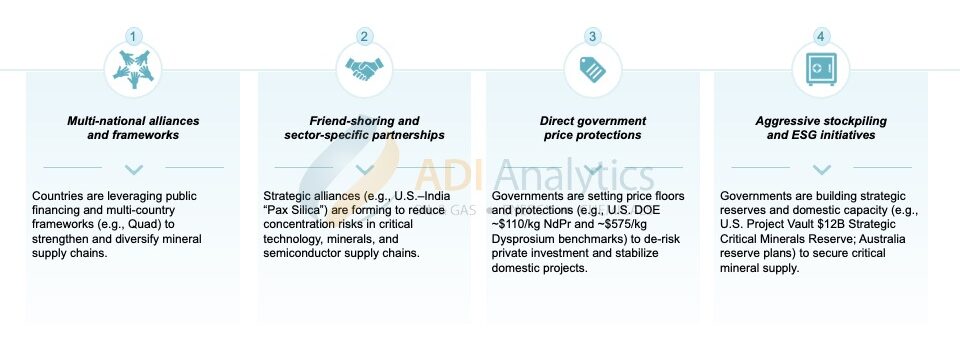

Against this backdrop, ADI is tracking a clear set of government-led initiatives emerging as a central theme in reshaping the critical minerals ecosystem. Governments are:

- Leveraging multinational alliances and frameworks, such as the Quad (or Quadrilateral Security Dialogue, an alliance between Australia, India, Japan, and the U.S. focusing on maritime security and critical technologies), to mobilize capital and diversify supply chains away from concentrated sources

- Advancing friend-shoring strategies and sector-specific partnerships, including bilateral initiatives like “Pax Silica,” led by the U.S. and joined by 14 countries to reduce geopolitical exposure

- Introducing price protection mechanisms, such as price floors (e.g., U.S. DOE’s ~$110/kg price floor for NdPr and ~$575/kg price floor for Dysprosium), to de-risk private investment and stabilize domestic project economics

- Implementing aggressive stockpiling and supply security measures, including large-scale reserves like “Project Vault” by the U.S. and similar initiative by Australia, to ensure long-term access

Collectively, these coordinated efforts signal a structural shift toward supply chain resilience and national security prioritization. Exhibit 1 summarizes key government initiatives to develop localized critical mineral supply chains.

Exhibit 1. Government initiatives to develop local critical minerals supply chain.

In parallel, companies across the value chain are responding with equally decisive actions—forming another key theme identified by ADI in navigating critical minerals supply bottlenecks. Mining companies, refiners, and downstream players are increasingly:

- Pursuing vertical integration and strategic partnerships to secure supply

- Making direct investments in upstream assets to build integrated value chains

- Developing integrated mine-to-magnet capabilities outside China

For example, companies are pursuing vertical integration and partnerships, as demonstrated by Energy Fuels, which has proposed a U.S.-controlled rare earth supply chain through its acquisition of ASM and plans to produce 6,000 tons per year (tpa) of NdPr by 2028. Similarly, firms are making direct upstream investments to build integrated value chains, such as Ioneer’s fully permitted “shovel-ready” lithium-boron project in Nevada, supported by $1 billion in U.S. government debt financing.

At the same time, players are advancing fully integrated mine-to-magnet capabilities, exemplified by USA Rare Earth’s acquisition of the Serra Verde asset, positioning it as the only fully integrated mine-to-magnet operator outside China. In addition, companies are leveraging government-backed financing to accelerate domestic capacity, such as MP Materials securing $400 million in U.S. Department of Defense funding to support rare earth magnet independence.

Overall, the industry is undergoing a broader realignment, where supply chain control and technological differentiation are becoming critical competitive advantages. Exhibit 2 showcases key company investments across the critical minerals value chain outside China.

Exhibit 2. Company initiatives to develop critical minerals supply chain outside China.

Building on these policy tailwinds and demand drivers, ADI sees a widening set of opportunities emerging across the critical minerals value chain, informed by its ongoing work with producers, investors, and downstream players. For miners and producers, assets once considered sub-economic are becoming increasingly viable, particularly where policy support, pricing visibility, and downstream integration can be leveraged. However, success still hinges on disciplined asset selection and cost competitiveness. At the same time, a growing pipeline of infrastructure and project financing opportunities is attracting investor interest with those leveraging ADI for due diligence and feasibility studies finding a rich set of opportunities to evaluate, increasingly focused on supply chain positioning and long-term offtake security. For industrial and chemical players, localized and integrated supply chains are opening new adjacencies in processing, refining, and enabling technologies, while end users must navigate a more complex sourcing landscape that balances security, cost, and performance. Across the board, the ability to translate market insight into execution is becoming a key determinant of success.

– Panuswee Dwivedi

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.