SLB this week agreed to acquire S&P Global Energy’s upstream software portfolio, aiming to bring software-like economics to OFSE companies. The acquisition includes the widely used Kingdom, Petra, and Harmony geoscience and petroleum engineering tools, mainly used for U.S. onshore workflows. SLB sees this as an expansion of its digital platform with essential tools to unlock upstream data value through its Lumi platform and Tela agentic AI framework. This deal comes as exploration spend and effort is rebounding across oil & gas majors and large E&P independents.

ADI has been active across the oil & gas software and digital landscape for more than a decade leading diligence on oilfield software targets for OFSE majors, strategic planning for E&P software players, and M&A strategy work for industrial software players. Collectively, the following themes stand out on digital and software growth across upstream oil & gas:

1. OFSE companies are expanding digital capabilities in the pursuit of software like revenue streams

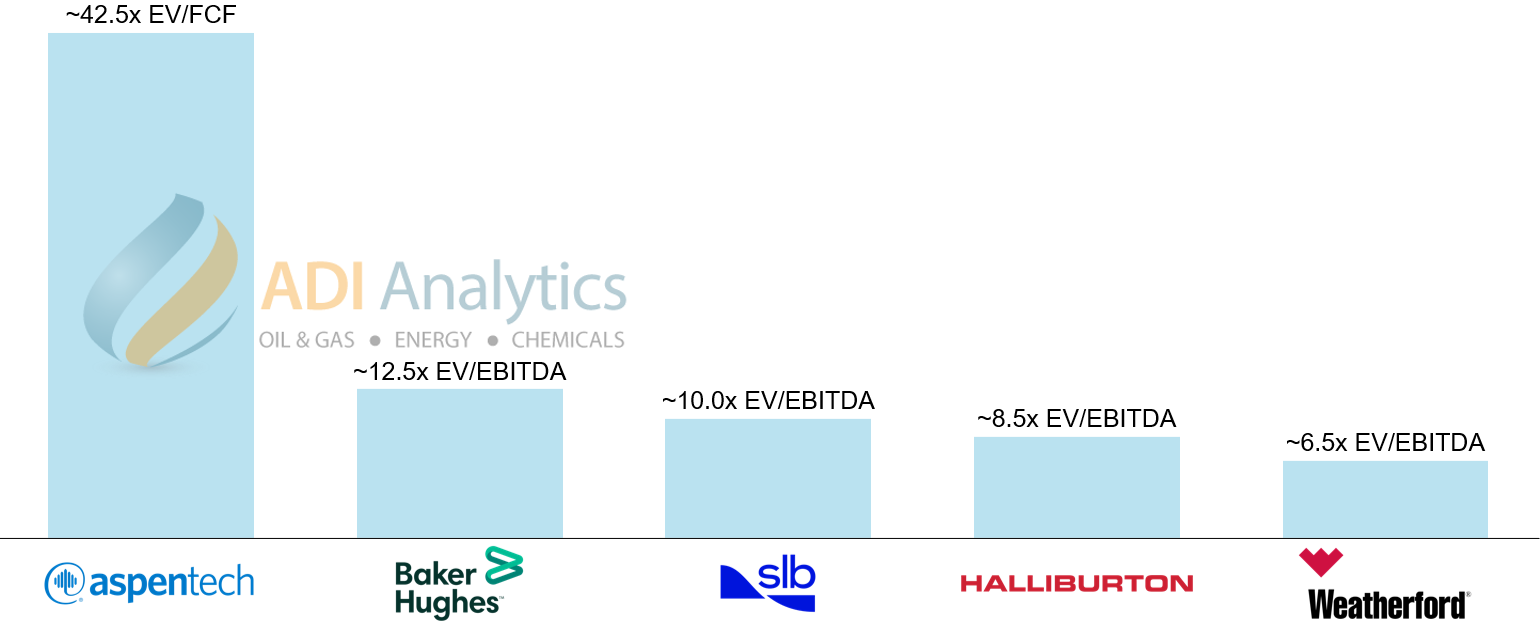

SLB’s Digital business posts software like profitability, achieving an adjusted EBITDA margin of 42% in late 2025. The business has surpassed $1 billion in annual recurring revenue as it migrates users toward SaaS models on Delfi. The goal is a larger share of recurring, capital light earnings that support durable cash generation even when activity normalizes. Such revenue quality will matter even if the market never values OFSE companies like a pure play industrial software business; for comparison, AspenTech commands ~42.5x EV/FCF while SLB trades at ~10.0x EV/EBITDA as shown in exhibit 1.

Exhibit 1. Target valuation multiples for AspenTech and leading OFSE players.

SLB’s peers are also pursuing other pathways to the same destination: Baker Hughes is building around field production automation and industrial adjacency with Leucipa deployed across ~75,000 wells globally. Weatherford is modernizing legacy production optimization through cloud migration and lifecycle analytics via an AWS partnership, expanding the ForeSite/CygNet ecosystem. Finally, Halliburton has emphasized automation embedded in execution systems such as LOGIX’s closed loop geosteering with ExxonMobil in Guyana, which finished 15% ahead of schedule.

2. Exploration spend is rebounding but organizational capabilities have weakened

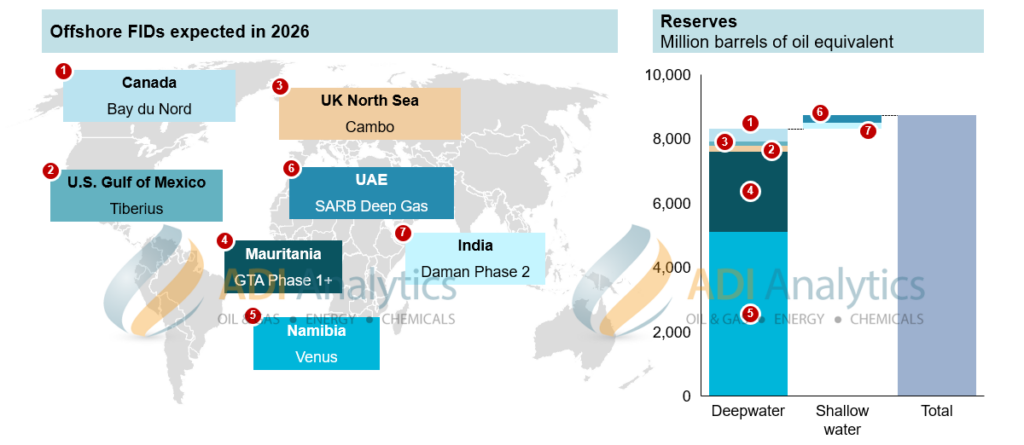

Exploration is regaining priority in many portfolios as companies seek to replenish reserves. Chevron is accelerating its efforts in Venezuela, Egypt, and the Gulf of Mexico, and adding offshore exposure near Greece and Libya. ExxonMobil has outlined a potential plan to invest up to $24 billion in Nigeria deepwater. An indication of this is the growing expectation of offshore FIDs globally, for instance, FIDs worth 8.8 billion barrels of oil equivalent are expected in 2026 as shown in exhibit 2.

Exhibit 2. Offshore FIDs expected globally in 2026 in million barrels of oil equivalent.

This backdrop also matters at the organization level. Several operators reduced exploration staffing during the long capital discipline period. As a result, internal exploration capabilities have weakened; Chevron is a notable example where its CEO has publicly voiced frustration with exploration results. Software that improves repeatability in planning becomes more relevant when institutional memory thins, and technical teams now require more “hand-holding” from software to make corrections.

3. Shale maturity increases the value of subsurface learning cycles

The shale patch is maturing rapidly and operators will no longer be able to rely entirely on incremental improvements in well design. Deepening subsurface understanding is becoming essential as E&P operators pursue unconventional resources in new regions like Latin America and the Middle East.

EOG’s Dorado discovery is a concrete example of exploration led value creation inside a mature basin. EOG identified a 21 Tcf net resource potential by emphasizing technical data, including petrophysical logs and 3 D seismic, pausing activity to evaluate results and apply learnings as it moved down the cost curve. Software and digital tools that shorten subsurface learning cycles have a clearer role when the marginal barrel is more geology sensitive.

4. Even so, digital adoption remains constrained by workflow lock‑in, data friction, and change capacity

Digital adoption continues to be shaped by how engineers work and how organizations absorb change. Legacy platforms remain embedded, making displacement difficult; for instance, less than half of all E&P companies surveyed still report limited progress in their digital journeys.

ADI’s operator interviews show adoption is contingent on measurable performance improvements in materially relevant applications. Projects stall when the integration burden or “data contextualization”—making disparate industrial data usable for AI—requires too much manual intervention.

5. Digital growth is increasingly defined by consolidation, platform extension, and targeted AI

Upstream software markets favor consolidation because workflows are interconnected. SLB’s acquisition adds recognized tools like Kingdom and Petra adjacent to its modeling stack to build domain foundation models.

The next frontier is Agentic AI—goal-driven software like SLB’s Tela that autonomously monitors operations and adjusts processes rather than simply generating reports. Adoption improves when AI sits inside existing engineering workflows to reduce decision friction, rather than asking teams to adopt an entirely new way of working.

Conclusion

As the industry navigates this complex transition, ADI Analytics helps digital players and industrial companies identify and capture growth opportunities through deep market research and strategic advisory. Whether conducting commercial due diligence on emerging software targets, developing go-to-market strategies for digital platforms, or benchmarking competitive landscapes, ADI provides the domain expertise necessary to bridge the gap between traditional industrial operations and the next generation of digital transformation.

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.