Specialty metallocene resins have emerged as a resilient bright spot in a structurally oversupplied petrochemical landscape where standard polyolefins face historically low margins at a 15-year trough. Driven by our ongoing market tracking and newly updated Multi-Client Study on Global Polyolefin Elastomers and Plastomers, ADI Chemical Market Resources has mapped three critical trends reshaping the current mPOE and mPOP market compared to our baseline data from three years ago:

1. Solar and EVs have shifted from incremental to primary demand engines

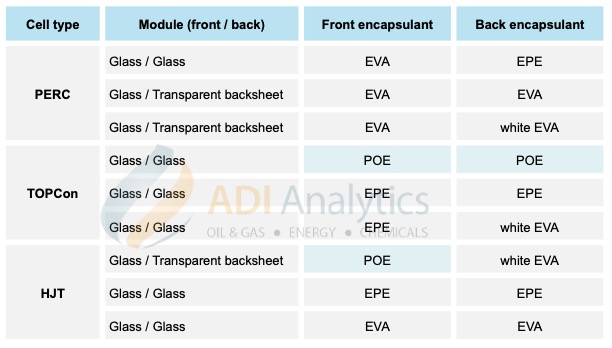

The core market driver has fundamentally pivoted. The rapid industrial transition to high-efficiency N-type solar cells (like TOPCon) saw their market share explode from 15% to over 60% in just two years. Because N-type cells are highly sensitive to moisture, mPOE has shifted from a niche alternative to the preferred encapsulation material over EVA due to its superior moisture barrier and lower potential-induced degradation (PID) risk, as shown in exhibit 1. Concurrently, automotive lightweighting and EV components—such as battery packaging and cable insulation—provide a strong second leg of demand, while hot-melt adhesives (HMAs) maintain a consistent, margin-accretive pull.

Exhibit 1. Choice of solar encapsulant by type of solar cell.

2. Supply dynamics have flipped to China expansion vs. rest-of-world rationalization

Three years ago, China relied almost entirely on imports for its POE needs. Today, it is aggressively localizing capacity to achieve import substitution. New domestic producers like Sierbang Petrochemical (bringing online a 100,000 tons per annum plant) and Wanhua Chemical are scaling integrated capabilities. In stark contrast, the rest of the world is rationalizing capacity amid the broader chemical downturn. Over 1 million metric tons of ethylene capacity has gone offline in Europe, South Korean producers are trimming naphtha cracking capacity, and structural portfolio shifts—such as SABIC’s recent asset sales—reflect a global pivot toward stricter investment discipline.

3. Pricing is dictated by geopolitical volatility, not just specialty tightness

The pricing environment has shifted from soft to highly volatile. While mPOE and mPOP retain a structural specialty premium, absolute prices remain tightly bound to base polyolefin and ethylene feedstocks. For example, a major supply shock via logistics disruptions in the Strait of Hormuz in early 2026 triggered sudden feedstock constraints, driving sharp, temporary spikes in blended average selling prices across the derivative polymer chain.

To optimize your product mix and successfully navigate future oversupply risks as new capacities scale, leverage ADI Analytics’ deep proprietary modeling. View our latest Global POE/POP Demand Forecast or contact our team today to see how our tailored strategic consulting can position your business for the next phase of the polyolefins cycle.

– Panuswee Dwivedi

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.