Over the past two years, EPC firms have begun talking about process technology licensing in a materially different way. In corporate filings, expert calls, and investor communications, licensing is no longer positioned as an adjunct to project execution. Instead, it is increasingly framed as a core strategic lever—one that delivers capital light margins, recurring revenue, and a way to participate in projects while limiting exposure to the risk profile of lump sum EPC contracting.

This shift is visible across refining, petrochemicals, and energy‑transition markets. EPCs such as Technip Energies, Toyo Engineering, JGC, Sinopec Engineering Group, and Engineers India Ltd. are all emphasizing proprietary technology portfolios, integrated licensor‑EPC models, or selective licensing‑only participation. ADI Analytics’ voice‑of‑customer and market work suggests this reflects a deeper re‑allocation of value across the petrochemical project lifecycle.

Below are five key insights that explain what is changing—and why it matters.

1. Technology licensing is being repositioned as a core profit engine

EPC firms increasingly describe technology licensing as a way to improve margin quality and earnings stability in an otherwise cyclical, risk‑heavy business. Rather than relying solely on lump‑sum turnkey execution, licensing is positioned as a capital‑light revenue stream that can generate recurring income and smooth earnings volatility.

This narrative is explicit in how EPCs now discuss their portfolios. Technip Energies, for example, highlights its Technology, Products & Services segment as a central growth driver across LNG, ethylene, and carbon capture. Sinopec Engineering Group has similarly emphasized the growth of its proprietary technology and licensing contracts as a contributor to research profitability and broader EPC competitiveness.

ADI’s work indicates that this repositioning is structural, not opportunistic. EPCs are investing in process IP, catalysts, and proprietary know‑how with the explicit goal of capturing value earlier in the project lifecycle and retaining it beyond construction.

2. Licensing decisions are becoming selective rather than demand‑driven

Market growth alone is no longer sufficient to justify licensing investment. Across methane‑, ethylene‑, and propylene‑based value chains, ADI’s analysis shows that licensing attractiveness varies widely depending on market structure, competitive intensity, and openness to new entrants.

In several large‑volume product chains, growth is accompanied by highly concentrated licensor positions, strong incumbency advantages, and limited willingness by producers to switch technologies. In these cases, EPCs see limited strategic upside from entering licensing markets late.

Conversely, some smaller or mid‑scale derivatives attract disproportionate interest because they combine ongoing capacity additions with more fragmented or evolving licensing landscapes. This divergence explains why EPCs increasingly rely on structured screening frameworks rather than headline demand growth when prioritizing licensing opportunities.

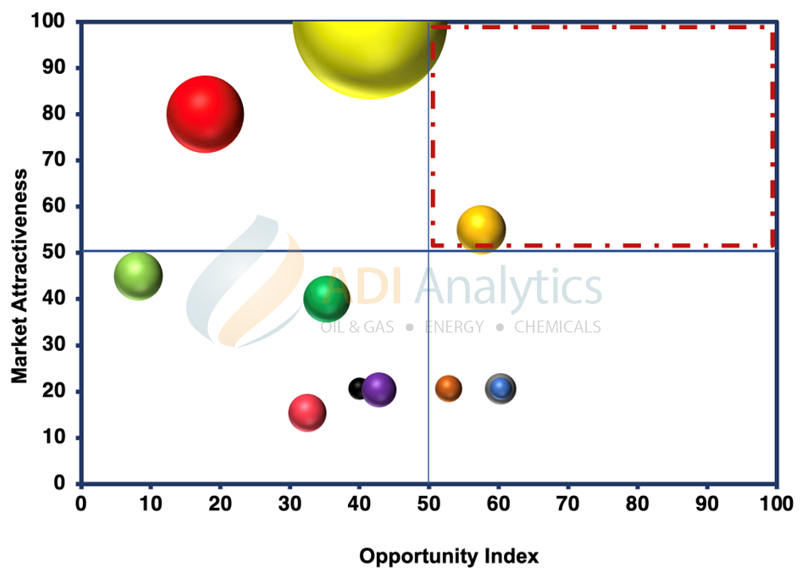

ADI has advised several EPC companies and process technology licensors on analyzing various markets using structured analytical approaches to prioritize the market segments with the best opportunities. Exhibit 1 is an illustrative example of our firm’s proprietary opportunity index and market attractiveness methodology to identify promising opportunities in key markets and value chains.

Exhibit 1. Illustrative example of ADI Chemical Market Resources’ proprietary opportunity index and market attractiveness analysis to identify best opportunities (represented by the spheres) in key markets and value chains.

The result is a clear shift: licensing opportunity often diverges from simple demand rankings, particularly in mature commodity chains.

3. Process route choice is reshaping competitive positioning

Licensing strategy is increasingly shaped by process route selection, not just end‑product demand. ADI’s work across multiple value chains shows that alternative or emerging routes can materially change competitive dynamics, even in otherwise mature markets.

EPCs now explicitly evaluate whether multiple viable routes exist, how route choice affects feedstock flexibility and cost position, and the extent to which proprietary catalysts create long‑term customer lock‑in. This is particularly evident in syngas‑based routes, ammonia, methanol, and emerging sustainable fuels.

Firms such as KBR and Technip Energies have publicly emphasized building technology portfolios around specific routes rather than broad molecule coverage. From ADI’s perspective, this reflects a tighter coupling between technology roadmaps and licensing strategy, with route selection treated as a strategic decision rather than a downstream engineering choice.

4. Integrated licensor‑EPC models are gaining traction

A notable shift in recent years is the growing emphasis on integrated licensor‑EPC offerings, where a single firm provides the core process technology and supports the project from early design through execution.

EPCs such as Engineers India Ltd. and Technip Energies routinely highlight their ability to act as a single point of responsibility across FEED, licensing, and EPC. ADI’s voice‑of‑customer research suggests this model resonates with producers seeking clearer accountability and tighter integration between process design and execution.

At the same time, some EPCs are selectively limiting their role to licensing only. Toyo Engineering, for example, has indicated a preference for participating in certain markets—such as green methanol or projects in North America—through technology licensing and related services rather than full EPC execution, explicitly to manage labor, supply‑chain, and cost‑overrun risk.

5. Barriers to entry determine whether licensing is scalable or niche

Technology licensing markets differ sharply in how open they are to new participants. In some product chains, a small number of licensors dominate global capacity additions, supported by strong IP positions and entrenched producer relationships. In others, multiple licensors, EPC‑affiliated technologies, or regional differentiation create room for entry.

ADI’s work highlights that understanding these structural barriers is critical before committing resources to licensing development. Key questions include how many licensors actively compete, whether licensing is bundled with catalyst supply or EPC execution, and how producers perceive switching risk over the asset life.

These factors often determine whether licensing represents a scalable growth platform or a niche capability best pursued selectively. EPCs that misread these dynamics risk investing heavily in licensing positions that never achieve meaningful scale.

What this means going forward

As petrochemical investment becomes more selective and capital discipline tightens, technology licensing is playing a more central role in how EPCs and technology holders compete. The shift underway is not about doing more licensing everywhere, but about doing licensing where it reinforces differentiation, improves risk‑adjusted returns, and strengthens long‑term positioning.

For EPCs, this means narrowing focus to technologies that align with execution strengths and strategic priorities. For technology holders, it underscores the importance of aligning licensing models with evolving customer expectations, competitive dynamics, and project risk profiles.

The firms that succeed will be those that treat technology licensing not as a support function, but as a deliberate, portfolio‑level strategy for value creation.

– Uday Turaga

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.