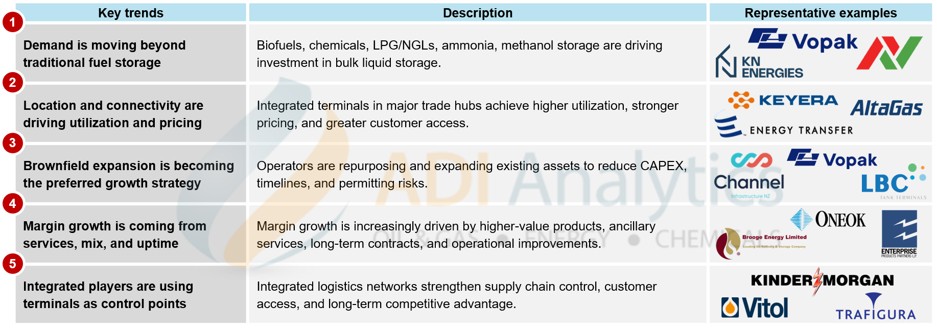

Liquid bulk storage operators are entering a more selective growth cycle. Demand remains resilient across fuels, chemicals, liquefied petroleum gas (LPG), natural gas liquids (NGLs), biofuels, ammonia, and methanol. Increasingly, value is shifting toward terminals that can handle a broader range of products, connect to major trade routes, and generate higher returns from existing assets.

Here are five trends shaping the future of the liquid bulk storage industry (see Exhibit 1):

Exhibit 1: Key trends shaping the liquid bulk storage industry

1) Demand is moving beyond traditional fuel storage

Refined products remain the industry’s foundation, but growth is increasingly concentrated in products requiring specialized infrastructure. Chemicals, LPG, NGLs, biofuels, renewable feedstocks, ammonia, and methanol each require different tank designs, coatings, heating systems, vapor management, material compatibility, and safety procedures.

Recent investments reflect this shift. For instance, Royal Vopak is investing ~$82 million to add 272,000 cubic meters of biofuel storage in Malaysia while developing ammonia import infrastructure in Europe and Japan. Aegis Vopak Terminals has expanded LPG capacity 4.5 times since 2021 to 225,800 metric tons and is constructing India’s first independent cryogenic ammonia terminal. KN Energies is expanding infrastructure for used cooking oil (UCO), sustainable aviation fuel (SAF), and methanol transshipment.

Many of these developments build on themes previously discussed by ADI’s analyst Edmund Lam in an article published in Tank Storage Magazine (Winter 2025/26 edition), which examined how the growing adoption of alternative fuels is driving new storage infrastructure requirements and reshaping terminal investment decisions.

The acquisition of LBC Tank Terminals by Mitsui O.S.K. Lines further illustrates where value is moving. LBC operates nearly 3 million cubic meters of storage across the U.S. Gulf Coast and ARA, with more than 70% of its revenue generated from chemicals and average utilization exceeding 90%.

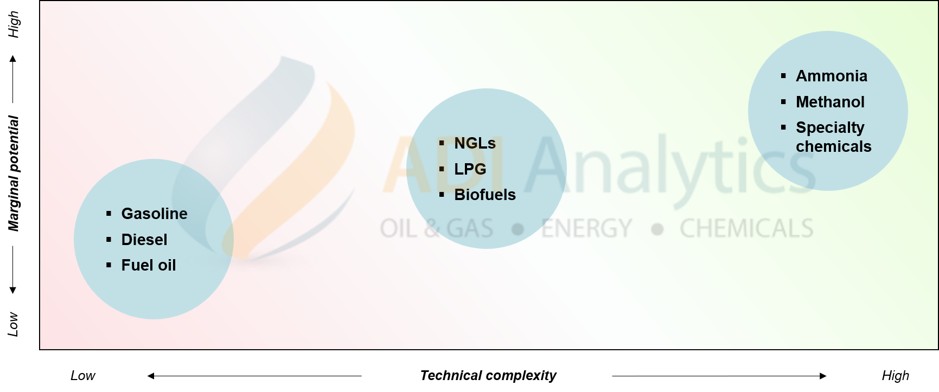

Product flexibility is becoming a greater source of value than fuel storage capacity alone. Operators must increasingly determine which molecules justify tank conversions, infrastructure upgrades, and long-term commercial commitments. As shown in Exhibit 2, products requiring more specialized storage infrastructure generally offer greater opportunities for value creation.

Exhibit 2: Relative market attractiveness of liquid bulk storage products

2) Location and connectivity are driving utilization and pricing

Storage assets generate the highest returns when positioned within major trade corridors. Hubs such as Amsterdam-Rotterdam-Antwerp (ARA), Singapore, and Fujairah combine marine access, industrial demand, trading activity, pipelines, and logistics infrastructure, consistently achieving utilization above 90%. Fujairah alone supports ~11 million cubic meters of independent storage capacity.

The same trend is evident in North American export infrastructure. Energy Transfer’s Nederland terminal provides more than 30 million barrels of crude storage with direct connectivity to Mont Belvieu. Its Flexport expansion added up to 250,000 barrels per day (bpd) of NGL export capacity, supported by long-term customer commitments extending into the 2040s. Marcus Hook complements this with 400,000 bpd of NGL export capacity and approximately 6 million barrels of storage.

Connectivity itself has become an investment theme. AltaGas and Vopak are developing the Ridley Island Energy Export Facility (REEF), adding 56,000 bpd of export capacity in Western Canada. Keyera, AltaGas, and CN are building the ACE Rail Terminal to connect Alberta NGL production with West Coast export terminals, while Adani Ports continues expanding liquid bulk infrastructure around India’s industrial and maritime hubs.

The value proposition now extends beyond storage. Operators are building integrated logistics systems that combine tanks, docks, pipelines, rail, and export infrastructure.

3) Brownfield expansion is becoming the preferred growth strategy for terminal operators and infrastructure investors

Greenfield terminals face longer permitting timelines, higher construction costs, and greater commercial risk. Industry participants increasingly cite six- to seven-year development timelines for major greenfield projects, while brownfield and modular expansions can often be completed within three to five years.

Refinery-to-terminal conversions illustrate the economics. Channel Infrastructure’s conversion in New Zealand required ~$57 million while preserving existing tanks, docks, and pipeline connectivity. The project also reduced operating costs and released hundreds of millions of dollars in refinery working capital.

Royal Vopak is repurposing capacity for pyrolysis oils, vegetable oils, biofuels, and other higher-value products, with a long-term objective of converting 30%–40% of its global oil hub capacity. LBC Tank Terminals is expanding at Rotterdam, Houston, and Lillo, while Petrobras and other operators are prioritizing expansions of existing facilities over new developments.

Capital allocation is becoming increasingly focused on identifying existing assets that can support future demand with the lowest capital and permitting risk.

4) Margin growth is coming from services, product mix, and operational excellence

While storage fees provide stable revenue, margin expansion increasingly comes from product mix, ancillary services, commercial structures, and operational performance.

Long-term contracts remain the foundation. Approximately 80% of Vopak’s revenue is protected by take-or-pay agreements, with nearly 90% of its industrial storage contracts extending beyond 10 years. Kinder Morgan reports that roughly 70% of its liquids terminal contracts follow similar structures.

Ancillary services provide additional revenue streams. Brooge Energy generates more than 40% of terminal revenue from blending, heating, and transfer services. Aegis Vopak expects average liquid storage tariffs to increase from $25 to $28 per cubic meter as chemicals become a larger share of its portfolio. At many chemical terminals, storage accounts for roughly 70%–75% of revenue, with the balance generated from heating, blending, loading, and related services.

Operational improvements are becoming equally important. ONEOK expects the Magellan acquisition to reduce butane logistics costs from ~$0.20 to $0.10 per gallon across more than 50 blending locations. Enterprise Products has invested in vapor recovery systems that capture hydrocarbons otherwise lost during loading, while many operators are deploying automation, predictive maintenance, and digital twins to increase throughput and reduce downtime.

For many operators, the greatest margin opportunities now come from improving existing assets rather than adding new capacity.

5) Integrated players are using terminals as strategic control points

Storage assets are increasingly becoming part of broader logistics and trading networks.

Enterprise Products Partners continues expanding infrastructure integrated with its pipeline, fractionation, and storage network. Kinder Morgan operates 136 liquids and bulk terminals with ~135 million barrels of storage, while Navigator Holdings and Enterprise jointly operate the Morgan’s Point ethylene export terminal, linking storage, shipping, and export demand.

Commodity traders are following similar strategies. Through Puma Energy, Trafigura controls ~ 60 storage terminals with 3.1 million cubic meters of capacity and has invested in export infrastructure in Argentina to strengthen regional crude flows. Vitol continues expanding its LNG and terminal portfolio, including participation in the Delfin LNG project.

Joint ventures are also becoming more common. The REEF partnership between Vopak and AltaGas is supported by long-term take-or-pay agreements, including a 15-year contract with Keyera.

These integrated models give operators greater control over logistics, exports, and trading optionality. Independent terminal operators increasingly need differentiated assets, advantaged locations, or specialized capabilities to remain competitive.

Outlook

The liquid bulk storage industry is becoming more specialized, better connected, and increasingly operationally sophisticated.

The strongest operators are repurposing tanks for higher-value products, strengthening connectivity to major trade flows, expanding ancillary services, and securing long-term contracts for products requiring more complex handling. Capacity remains important, but the greater challenge is identifying which assets will remain competitive as products, trade flows, and customer requirements continue to evolve.

– Uday Turaga and Edmund Lam