The coatings, adhesives, sealants, and elastomers (CASE) sector is in the middle of a structural reset. What was once a market defined by steady, incremental growth is now being reshaped by multi‑billion‑dollar mergers, aggressive portfolio pruning, and a widening gap between scale leaders and specialized innovators. As diversified chemical companies separate high‑value specialty businesses from commoditized core operations, a new industry map is emerging—drawn jointly by global strategic consolidators and increasingly sophisticated private equity sponsors.

ADI has been active in the CASE M&A market for many years and continues to follow it closely. We’ve recently refreshed our proprietary landscape of the global CASE market and participant landscape and see five key findings shaping how capital is being deployed and where value creation is increasingly concentrated:

Key finding 1: Extreme scale has become a primary driver of valuation expansion

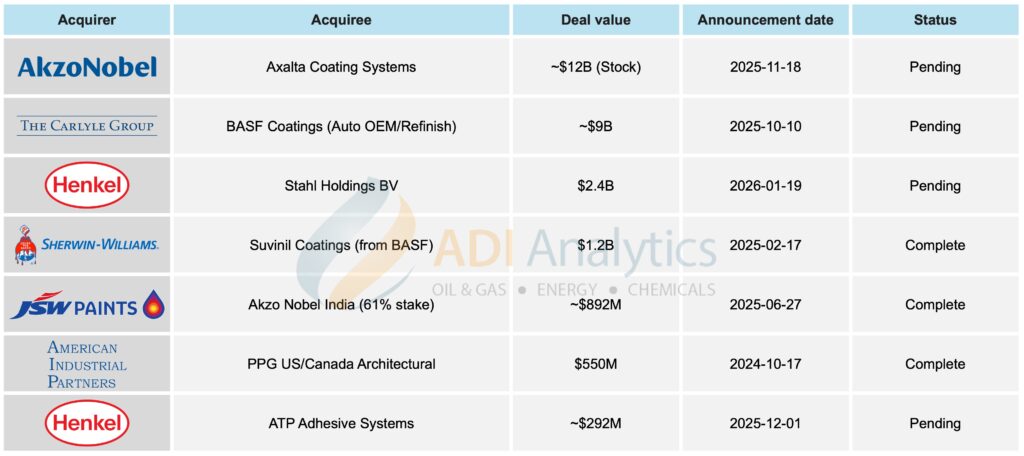

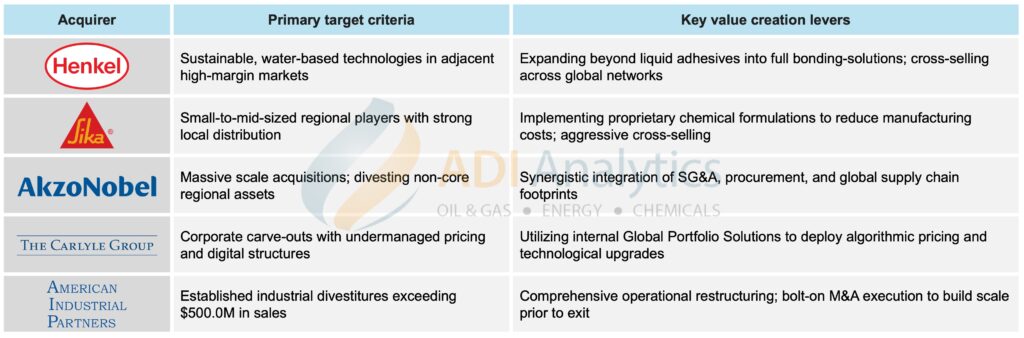

The clearest signal of the sector’s new direction is the proposed $25.0 billion merger of equals between AkzoNobel and Axalta, which would create a global coatings leader with $17.0 billion in combined annual revenue. The strategic logic is explicit: management teams now view extreme scale as one of the few remaining levers for sustained valuation multiple expansion in mature CASE markets.Beyond headline size, the merger is expected to unlock roughly $600 million in run‑rate synergies, driven by procurement leverage, footprint rationalization, and SG&A efficiency. More importantly, scale enhances price discipline and customer coverage across refinish, industrial, and mobility end markets—advantages that are increasingly difficult to replicate organically. Exhibit 1 describes the primary target criteria of various acquirers in CASE markets.

Exhibit 1. Primary target criteria of various acquirers in CASE markets.

Key finding 2: Portfolio pruning is accelerating as giants exit non‑core assets

Parallel to mega‑mergers, large chemical companies are aggressively simplifying portfolios. BASF’s €7.7 billion carve‑out of its automotive OEM and refinish coatings business to Carlyle and PPG’s $550 million divestiture of its U.S. and Canadian architectural coatings unit to American Industrial Partners (AIP) exemplify a broader trend toward monetizing mature or volatile businesses.

These transactions reflect a shift away from sprawling, diversified models toward more focused specialty platforms. For sellers, divestitures unlock trapped value and recycle capital. For buyers—particularly private equity—these assets offer immediate scale, established brands, and multiple levers for operational improvement. Recent major transactions across the CASE landscape are summarized in Exhibit 2.

Exhibit 2. Recent M&A deals and strategic transactions in CASE markets.

Key finding 3: M&A is increasingly about high‑margin technological adjacencies, not just size

Deal rationales in the CASE sector are evolving beyond cost synergies toward product adjacency and customer embedment. Henkel’s acquisitions of ATP Adhesive Systems and Stahl are emblematic of this shift. Together, these assets move Henkel decisively beyond liquid adhesives into a “full bonding solutions” portfolio, spanning specialty tapes, flexible-material coatings, and surface treatment technologies.

These adjacencies matter because they are typically higher margin, more application‑specific, and more deeply integrated into customer workflows. This same logic is playing out regionally. Sherwin‑Williams’ acquisition of Suvinil positions the company as the dominant player in Brazil’s architectural coatings market, while JSW Paints’ $891.75 million majority acquisition of Akzo Nobel India underscores how local champions are consolidating fast‑growing infrastructure and housing demand in emerging markets.

Key finding 4: Mid‑market investors are scaling fragmented assets through buy‑and‑build strategies

Mid‑sized investors are navigating the market by pivoting toward the fragmented middle‑market landscape, specifically targeting companies with an enterprise value between $50 million and $500 million. By utilizing a buy‑and‑build strategy, these funds acquire foundational platforms and scale them through complementary bolt‑on acquisitions to capture market share.

Strategically, they are shifting toward asset‑light operating models in niche geographies to minimize capital risk, while deploying hands‑on operational improvements to drive organic growth. The primary implications of this approach include:

- The ability to exploit valuation arbitrage through inefficient price discovery

- A reliance on strategic sales or secondary buyouts for exits, given a sluggish IPO market

As a result, these investors increasingly function as specialized incubators—building, professionalizing, and de‑risking niche CASE assets that are ultimately sold to global strategic consolidators.

Key finding 5: Sustainability and IP depth are defining the next generation of winners

Looking ahead into 2026, M&A activity in the CASE sector remains robust but increasingly selective. The focus is shifting from pure cost synergies toward pricing and mix improvement, sustainability‑driven innovation, and regulatory resilience. Stricter regulations around VOCs and PFAS are accelerating demand for water‑based and bio‑based formulations, forcing acquirers to reassess legacy solvent‑heavy portfolios.

Sustainability has become a balance‑sheet issue, not just a marketing claim. Henkel’s ATP acquisition, for example, was strongly motivated by the fact that over 90% of ATP’s portfolio is water‑based, making it immediately accretive to Henkel’s sustainability and regulatory positioning.

Against this backdrop, attention is increasingly focused on mid‑sized and regional champions with deep IP moats, including:

- Aspen Aerogels (ASPN): Provider of proprietary PyroThin aerogel thermal barriers, already qualified by OEMs such as GM, Toyota, and Audi for EV battery thermal runaway protection

- Loar Holdings (LOAR): A premium aerospace supplier generating 85% of revenue from proprietary products, with EBITDA margins projected to approach 50% by 2026

- Astral Ltd: A dominant Indian regional champion consolidating specialty chemistries and rapidly expanding manufacturing capacity across India and the Middle East

Some of the other mid-sized and regional champions are enlisted in Exhibit 3 below.

Exhibit 3. Select mid-size and regional champions globally.

Closing perspective

The CASE sector is now a high‑stakes arena for technological differentiation and operational execution. As consolidation accelerates, the industry will likely be defined by a widening valuation gap between “green,” IP‑rich platforms and legacy solvent‑based incumbents. For investors and acquirers, the path to value creation increasingly requires a sophisticated blend of sustainable formulation, digital pricing discipline, and the operational grit needed to stand up complex independent businesses from the shells of old‑line conglomerates.

– Panuswee Dwivedi

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.