ADI has published nine editions of our semi-monthly newsletter, SAF Tracker, so far in 2026 covering trends across SAF demand, supply, pricing, technology, feedstocks, investments, and regulations. Stepping back from the cadence of biweekly reporting, we found ourselves asking a broader question: what are the high-level trends shaping the SAF landscape this year?

Our analysis reveals that the market is moving beyond early adoption into a more complex, compliance-driven phase marked by fragmentation, supply constraints, and caution. Five trends stand out as defining the SAF landscape so far in 2026:

- Regulatory rollbacks vs. enforcement

A sharp regional divergence is fragmenting the global market. While the United States faces economic pressure and policy uncertainty following the contraction of the 45Z clean fuel credit framework, the European Commission has aggressively reaffirmed its ReFuelEU Aviation mandates along with strict penalty structures—forcing a compliance-first mentality. - Geopolitical disruption of energy pricing

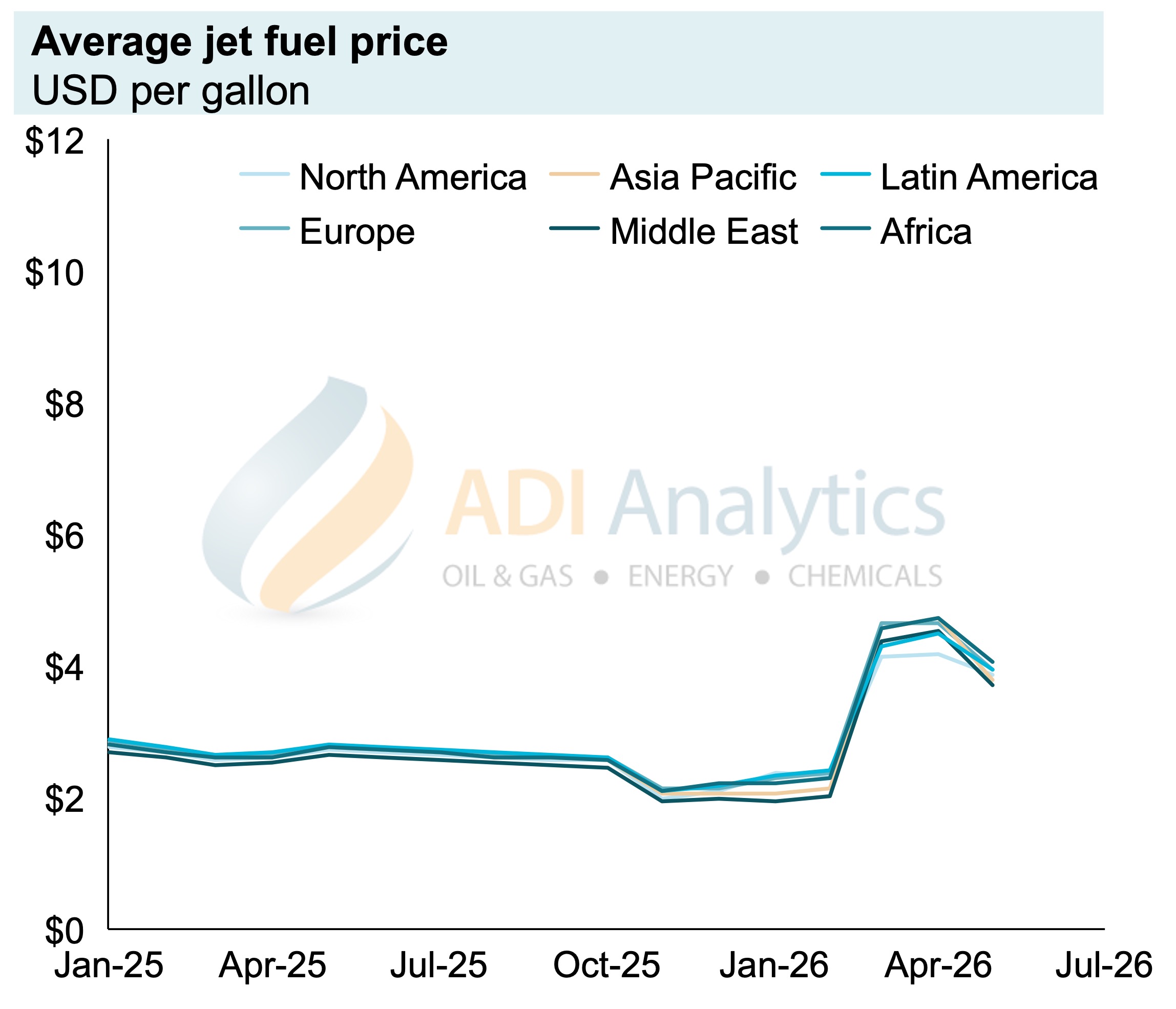

Recent trade disruptions and conflict in the Middle East have driven a dramatic spike in conventional jet fuel prices, which surged from roughly $2.00/gal to over $4.50/gal. This volatility has temporarily narrowed the green premium for SAF relative to fossil alternatives, fundamentally altering near-term airline margin planning. Exhibit 1. below shows jet fuel price trends through mid-May 2026.

Exhibit 1: Average jet fuel price by region (IATA).

- Diversification beyond HEFA

The dominant Hydroprocessed Esters and Fatty Acids (HEFA) pathway is approaching a physical ceiling due to constrained waste lipid and used cooking oil (UCO) supply. As a result, Alcohol-to-Jet (ATJ) and Power-to-Liquid (PtL) technologies are beginning to attract commercial investment as pathways to scalable growth. - The looming eSAF deficit

Despite ambitious European mandates requiring a 1.2% eSAF sub-quota by 2030, industrial scale-up remains significantly delayed. Capital-intensive value chains and a lack of final investment decisions (FIDs) point to a potential domestic European supply deficit of up to 244 million gallons by 2030. - Institutionalization of book-and-claim

Persistent infrastructure and supply chain bottlenecks have elevated book-and-claim systems into core market architecture. By decoupling environmental attributes from physical fuel molecules, these registries enable multinational corporations and cargo operators to meet Scope 3 emissions targets on a global basis.

These themes emerge directly from ADI’s ongoing SAF Tracker coverage, which continues to monitor developments in offtake agreements, project activity, pricing dynamics, and the evolution of policy. Taken together, they point to a market entering a more disciplined, but also more constrained phase of growth. To ensure success, companies will have to navigate policy asymmetry, secure advantaged supply, and adapt early to emerging technology pathways in what is quickly becoming a structurally tight and compliance-led market. ADI can help with these needs through our SAF Tracker publication or bespoke consulting work.

– Panuswee Dwivedi

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.