Part of ADI Analytics’ ongoing coverage of the implications of the Iran conflict across oil & gas, LNG, refined products, and chemicals.

On April 28, 2026, the United Arab Emirates (UAE) announced it was quitting the Organization of the Petroleum Exporting Countries (OPEC), the producer group created in 1960 to coordinate and unify petroleum supply policies among members. UAE had been a member of OPEC since 1967.

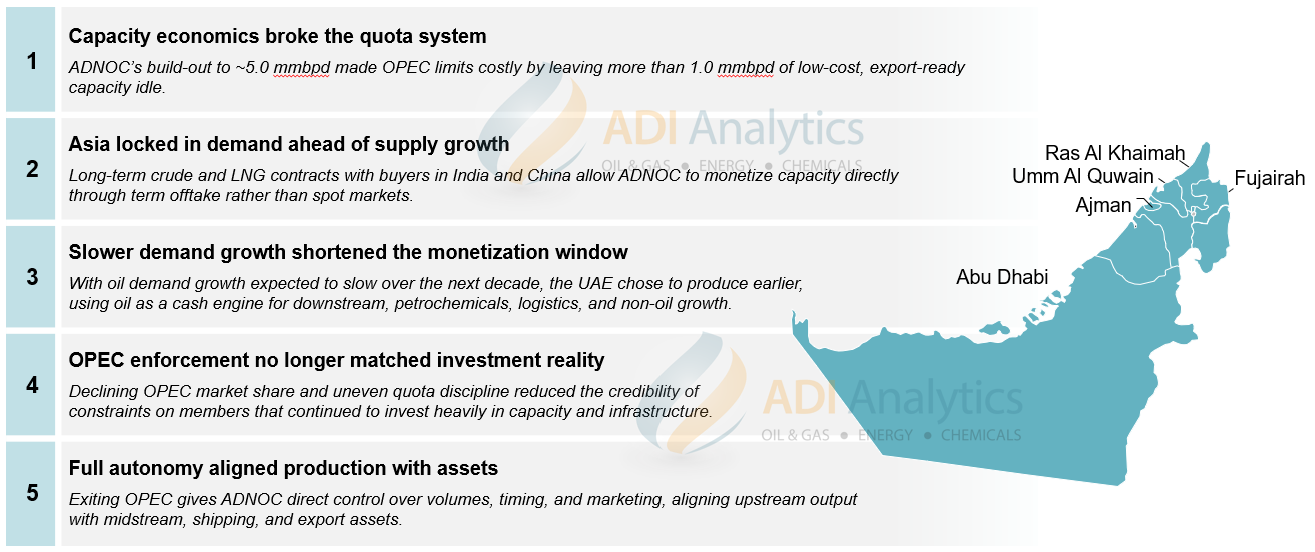

We see five structural drivers behind the UAE’s decision, centered on capacity economics, demand security, and control over long‑term monetization of its resources (see Exhibit 1).

Exhibit 1: Five structural drivers behind the UAE’s decision in leaving OPEC.

1. Low‑cost capacity makes quotas expensive

ADNOC is targeting around 5.0 million barrels per day of production capacity by 2027. OPEC quotas constrained output to roughly 3.8 million barrels per day, leaving more than 1.0 million barrels per day idle. At $60 oil, that foregone volume represents roughly $25–30 billion per year in gross revenue. At $100 oil, the figure moves toward $45–50 billion. ADNOC’s core assets—Upper Zakum, Bu Hasa, Bab, and Lower Zakum—sit well below global marginal cost, giving the UAE limited economic incentive to withhold supply.

2. Long‑term Asian contracts reduce reliance on spot pricing

The UAE has secured long‑duration demand across Asia, shifting more volume under term contracts. ADNOC Gas signed a 10‑year, ~$3 billion LNG supply agreement with Hindustan Petroleum in January 2026 for 0.5 mtpa, and Indian Oil committed in late 2024 to 1.0 mtpa for 15 years from the Ruwais gas project. Beyond LNG, ADNOC has tied crude marketing to downstream and storage investments in India, including strategic petroleum reserve capacity. These structures convert upstream capacity directly into predictable cash flow, reducing dependence on coordinated price management.

3. Transition timing favors producing sooner, not later

Global oil demand growth is slowing with growing risks that demand may peak or plateau within the next decade. For producers with fiscal breakevens near $50–60 per barrel, holding barrels underground carries rising opportunity costs. The UAE has increasingly treated oil as a cash‑generating asset to fund downstream expansion, logistics, chemicals, and non‑oil sectors, including the $45 billion Ruwais petrochemicals complex and broader industrial diversification.

4. OPEC’s ability to enforce discipline has weakened

OPEC’s share of global oil supply has fallen below 35%. Quotas increasingly limit members with capacity growth while doing little to restrain producers outside the group. The UAE was producing at roughly 70% of nameplate capacity, well below peers, creating a structural mismatch between investment and allowed output.

5. Independent production supports autonomy and flexibility

Leaving OPEC gives ADNOC full control over production, marketing, and timing. It allows the UAE to respond directly to market signals, align upstream growth with midstream and export capacity, and support ADNOC Logistics & Services, which already derives more than half its revenue from long‑term contracted volumes and plans to double throughput by 2030.

While other factors such as geopolitics may have also influenced the decision, the UAE’s exit is rooted more in economic drivers and is a move toward autonomy, volume efficiency, and long‑term monetization in a slower‑growth oil market. Even so, what does this mean for operators, oilfield service companies, energy equipment manufacturers, and investors? For example:

- When will we see ADNOC move into production growth? If the UAE increases production, will upstream investments slow elsewhere?

- Will oilfield services demand in the UAE rise meaningfully and when?

- How is midstream capacity — pipelines, storage, export routes — in the UAE positioned?

- Does upstream output impact downstream chemicals and petrochemicals where UAE has been investing heavily?

- Finally, what happens to the price of oil?

We will address these questions in a forthcoming blog.

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.