On April 7, 2026, the European Commission announced the first official Carbon Border Adjustment Mechanism (CBAM) certificate price for Q1 2026 at €75.36 per tonne of CO2 equivalent (~$88/t CO2e),markingthe EU’s first explicit carbon price applied to imported goods. This rate will be applied to the embedded emissions in CBAM-covered imports and is calculated from the weighted average clearing prices in EU Emissions Trading System (ETS) auctions from the previous quarter. In 2026, the certificate value will be updated quarterly, shifting to a weekly schedule in 2027 to ensure real-time alignment with the EU’s carbon market.

1) Steel, cement, and chemicals face immediate cost pressure

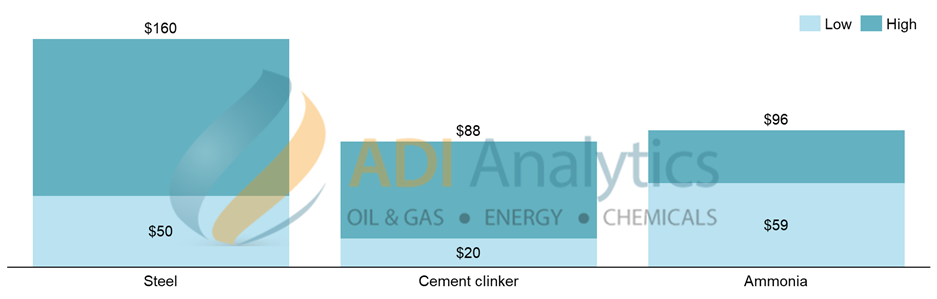

Steel and cement importers are expected to see the most immediate impact. For steel, the CBAM levy is estimated to add $50-$160 per tonne in 2026 (see Exhibit 1), depending on the carbon intensity of the production route. Cement imports from non-EU regions, where carbon intensity often exceeds EU levels (0.80-0.86 t CO2 per tonne versus the EU average of 0.78 t CO2 per tonne), face even steeper cost pressure.

The chemicals sector also faces significant disruption, particularly for foundational chemical products like ammonia and hydrogen. As ammonia plays a critical role in fertilizer production, CBAM-related carbon costs could add up to ~$100 per tonne for ammonia (see Exhibit 1), increasing overall fertilizer costs. While ammonia and hydrogen are currently most exposed, the scope is expanding quickly. More than 120 chemicals and polymers are already under assessment for potential inclusion by 2028, including methanol, olefins, and plastic resins.

Exhibit 1: Estimated CBAM cost impact on steel, cement, and ammonia ($ per tonne).

2) Accelerating the shift toward localized, lower-carbon supply chains

CBAM is reinforcing a structural shift already underway in global trade. By increasing the cost of carbon-intensive imports, the policy incentivizes production closer to end markets and in regions with cleaner energy systems. This is supporting demand for domestic or regional suppliers, as companies seek to reduce both carbon costs and administrative complexity. At the same time, export-oriented economies such as China, Turkey, and India may see their traditional cost advantage eroded as carbon intensity becomes a more decisive competitive factor.

EU importers will need to revisit sourcing strategies and develop supplier-level visibility on carbon emissions. Managing CBAM exposure will increasingly require a shift toward low‑carbon feedstocks such as green ammonia, low-carbon hydrogen (blue, green, and turquoise), and low-carbon cement. Likewise, non-EU suppliers will need to accelerate decarbonization of production routes and introduce certified low-carbon product offerings to remain competitive in EU market. Investments in climate technologies such as carbon capture and renewable energy procurement will be key levers for reducing emissions intensity and maintaining cost competitiveness.

3) Greenhouse gas (GHG) emissions data is becoming critical to cost competitiveness

Steel, cement, and chemical producers are being pushed to strengthen GHG emissions measurement, reporting, and verification (MRV) capabilities across the value chain to provide verified supplier-level emissions data. This could mirror trends seen in upstream oil and gas methane emissions monitoring, with increasing adoption of MRV technologies and methods such as satellite imaging, IoT-enabled sensors, AI/ML analytics, and third-party verification platforms such as MiQ.

Companies that cannot provide verified emissions data must rely on default values. These defaults are typically set at highly carbon‑intensive levels to act as a financial penalty for limited transparency. For example, a Turkish cement producer may report verified emissions of around 0.88 t CO₂ per tonne, while the default clinker intensity is set at 1.52 t CO₂ per tonne. That difference can translate into a cost gap of ~$58 per tonne, with costs of about $20 per tonne under verified data versus $88 per tonne under default assumptions. Default values will increase progressively, rising by 10% in 2026, 20% in 2027, and 30% from 2028 onward, further widening the gap between verified and unverified emissions.

4) CBAM pressures other regions to adopt carbon pricing

Countries such as China, where domestic carbon prices remain well below EU levels, face a clear policy decision, which is to either pay the carbon cost of exports to the EU through CBAM or implement domestic carbon pricing to retain that revenue locally. Brazil, Turkey, India, and several Southeast Asian countries, including Malaysia and Thailand, are actively developing carbon market frameworks and exploring the rollout of carbon taxes, particularly for emissions-intensive sectors such as chemicals and steel.

Although importers will only begin surrendering CBAM certificates in February 2027 to cover 2026 emissions, EU importers will need to start revisiting sourcing strategies and building supplier-level visibility on carbon emissions well in advance. At the same time, suppliers will need to accelerate decarbonization of production routes and introduce certified low-carbon product offerings to remain competitive in EU markets. While the European Commission has not yet released a comprehensive set of product- and country-specific default values, as many technical rules are still being finalized, the CBAM certificate price for Q1 2026 marks the first clear, quantifiable carbon tax for global trade. Over time, CBAM could act as a catalyst for broader adoption of carbon tax across jurisdictions.

– Edmund Lam

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.