We shared some of ADI Analytics’ research on methane emissions at the 5th Energy Emissions Management Conference in Houston last week. While the methane emissions measurement, reporting, and verification (MRV) landscape is clearly far more mixed today than a year ago, operators in 2026 continue to address material challenges around regulatory pressure, buyer requirements, and verification expectations. Broadly speaking, we at ADI Analytics see a clear set of structural shifts that will define how methane MRV evolves over the rest of the decade.

1. Regulatory gravity has shifted toward Europe, and exporters are aligning accordingly

Methane regulation is tightening where it most directly affects trade. The EU Methane Regulation embeds measurement‑based MRV, reconciliation, and third‑party verification requirements and extends them to imported oil and gas. Exporters selling into Europe increasingly design methane programs to meet EU expectations even when operating in jurisdictions with weaker federal requirements.

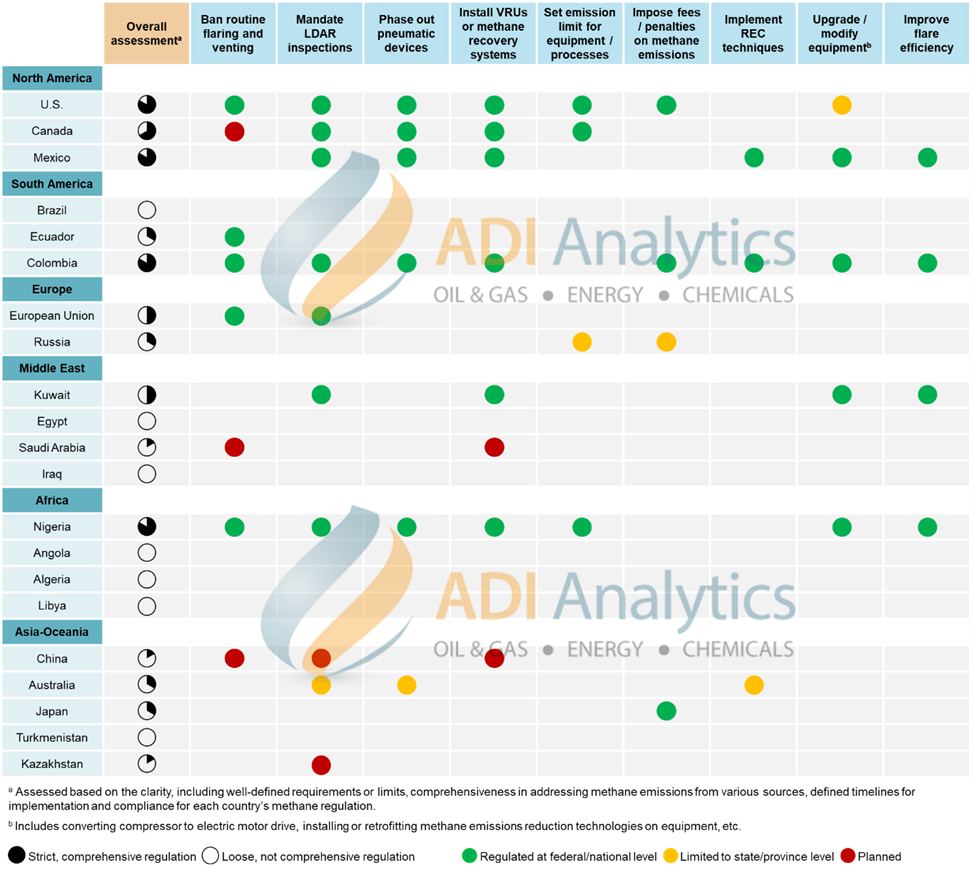

Over the years, ADI Analytics has closely tracked global efforts to regulate methane emissions, as illustrated in Exhibit 1. The following summarizes several of our key findings:

- EU rules require site‑level measurement, reconciliation of top‑down and bottom‑up data, and independent verification, with increasing scrutiny through 2030.

- Canadian methane regulations similarly emphasize measurement‑based approaches and aggressive reduction targets, reinforcing alignment with global frameworks.

- In the U.S., federal uncertainty has not translated into weaker practice for large operators; state‑level rules, investor expectations, and export exposure continue to sustain high‑standard MRV adoption.

- In other regions outside Europe and North America, regulatory action remains largely limited with countries such as Colombia and Nigeria are among the few leading methane emissions initiatives in South America and Africa, respectively.

Exhibit 1: Overview of methane emissions regulatory efforts by country.

(Source: ADI Analytics)

ADI Analytics’ benchmarking work shows that operators with EU exposure are already differentiating capital allocation and technology investment decisions based on whether assets can meet European methane expectations without bespoke workarounds.

2. Commercial markets are translating methane performance into contractability

Methane intensity is becoming a commercial attribute rather than a disclosure metric. Buyers, particularly in Europe, increasingly rely on certification and standardized scoring to differentiate supply.

- MiQ certification now covers a substantial share of U.S. natural gas production, creating a scalable mechanism for comparing methane performance across producers.

- Tourmaline achieved MiQ Grade A certification for an integrated production and processing system covering roughly 1.6 Bcf/d, signaling that certification is moving beyond pilots into core operations.

- Centrica Energy’s long‑term offtake agreement with Seneca Resources for certified gas demonstrates how methane performance is entering multi‑year commercial contracts rather than short‑term spot differentiation.

- LNG supply chains are beginning to apply full‑chain methane accounting, with pilots linking upstream U.S. production to European buyers.

ADI Analytics supports both sides of this market: helping operators understand where their methane intensity sits relative to peers, and helping MRV and certification providers size addressable markets and define customer segments as certification moves into mainstream procurement.

3. Measurement is being operationalized through layered monitoring systems

Methane measurement has shifted from periodic surveys to operational infrastructure. Leading operators deploy “systems of systems” that combine continuous monitoring, aerial surveys, and satellites, each serving a distinct purpose.

- Continuous monitoring systems are increasingly integrated into field operations, enabling faster detection and repair cycles rather than post‑hoc reporting.

- Aerial LiDAR platforms have demonstrated materially faster turnaround times, allowing operators to move from detection to action within days rather than months.

- Satellite systems are now routinely used for basin‑scale screening and super‑emitter identification, supporting independent verification and external credibility.

- Companies such as SM Energy have embedded real‑time methane signals into centralized operations centers, treating methane alongside production and reliability metrics.

From an advisory perspective, ADI Analytics increasingly works with operators on measurement strategy and technology roadmaps, helping them avoid over‑instrumentation while still meeting verification and regulatory thresholds.

4. Reconciliation has become the technical center of MRV credibility

Across frameworks, reconciliation has emerged as the defining technical requirement. The question is no longer whether emissions are measured, but how conflicting signals from different measurement layers are integrated into a single defensible emissions estimate.

- OGMP 2.0, MiQ, and Veritas all require explicit reconciliation between source‑level inventories and site‑level observations.

- Reconciliation decisions now drive reported methane intensity more than the choice of individual sensors.

- Differences in boundary definitions, temporal extrapolation, and treatment of below‑detection‑limit measurements explain much of the dispersion seen in operator benchmarking.

ADI Analytics’ methane benchmarking consistently finds that operators with similar assets can report materially different methane intensities based solely on reconciliation methodology. As a result, reconciliation governance, documentation, and repeatability are becoming executive‑level concerns rather than technical footnotes.

5. Verification readiness is emerging as the real bottleneck

As methane MRV moves into formal assurance, verification readiness is becoming the limiting factor for compliance and market access.

- EU‑linked methane reporting requires reasonable‑assurance verification by accredited third parties, with clear expectations around evidence trails, uncertainty treatment, and completeness.

- Interim verification protocols are already shaping how operators design inventories today, ahead of formal ISO‑linked standards expected later in the decade.

- Organizations that treat verification as a final compliance step face rework, delays, and credibility risk; those that build audit‑ready systems from the start move faster and with lower cost.

Operators will need support from specialists with verification‑oriented readiness work, including MRV system design, gap assessments against emerging assurance expectations, and development of traceable reconciliation workflows that improve audit readiness.

Where this leaves the market

Taken together, these shifts point to a methane MRV landscape that is consolidating around a small number of aligned frameworks, shared technical expectations, and increasingly standardized commercial signals. By the end of the decade, methane MRV will likely have made material progress to function much like financial reporting: built on common standards, subject to assurance, and directly linked to capital access and customer relationships. Operators that invest early in measurement strategy, reconciliation discipline, and verification‑ready systems are positioning themselves not just for compliance, but for sustained competitiveness in global gas and LNG markets.

– Piercen Hoekstra, Edmund Lam, and Uday Turaga

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.