North American midstream companies are entering a multi‑year transition as AI‑driven electricity demand reshapes how natural gas infrastructure is planned, financed, and contracted. Over the next five years, the sector is expected to evolve from linear pipeline expansion toward integrated power platforms that combine supply, transport, storage, and generation around large, fixed loads.

Several large midstream operators have already begun repositioning around this shift. For example, Williams and Energy Transfer are advancing pipeline, compression, and contracting strategies tied directly to data‑center and utility power loads, rather than traditional basin‑to‑market growth alone. Here are some key themes that we see going forward:

1. Power demand from AI and data centers is expected to anchor a multi‑year gas demand cycle.

Announced data center and other large‑load projects imply roughly 50 GW of incremental power demand tied to AI, which could drive ~7.5 Bcf/d of additional natural gas demand through 2030. This sits alongside longer‑dated structural drivers, including coal retirements across the Midwest and Great Lakes that are expected to create demand pull for an additional ~5 Bcf/d of gas by 2040. The result is a longer, smoother demand curve rather than a short‑cycle spike.

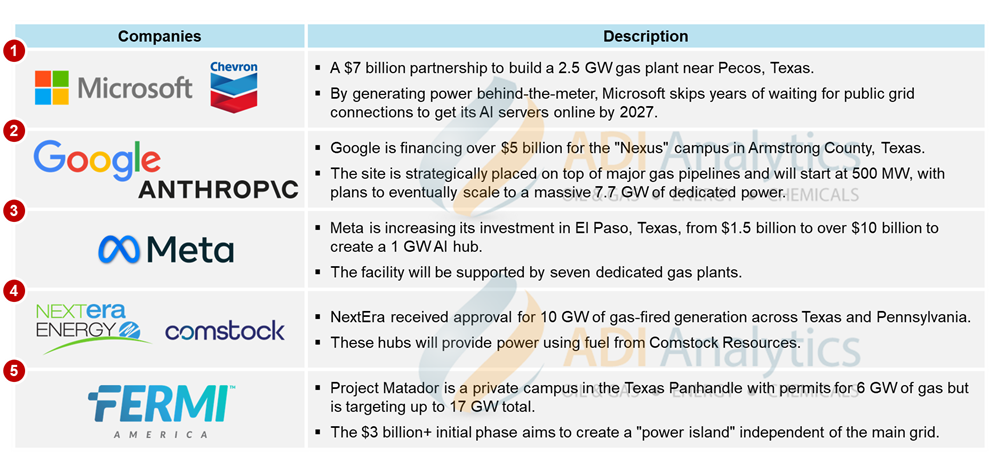

Exhibit 1: Recent data center natural gas power deals.

2. Behind‑the‑meter generation is likely to expand as a bridge, then persist as a feature.

Grid interconnection timelines exceeding four years in many markets are pushing hyperscalers toward on‑site or co‑located gas generation. Equipment availability is tightening as well. Lead times for large, high‑efficiency combined‑cycle turbines have extended to 3–5 years, reinforcing interest in modular and distributed solutions. Behind‑the‑meter strategies are already moving from concept to execution, with Williams committing capital to modular gas‑fired generation through its Power Innovation platform and Enbridge partnering with Bloom Energy to deploy on‑site power solutions for data‑center customers. Even as grid capacity eventually expands, behind-the-meter configurations are expected to remain in use where uptime, latency, or redundancy carry a premium.

3. Midstream platforms are likely to compete on their ability to deliver “power campuses.”

The next phase of development increasingly points toward clustered solutions that combine pipelines, storage, and generation into semi‑integrated campuses serving multiple large loads. This favors operators with scale, permitting depth, and balance sheets capable of executing multi‑asset projects. This campus-style approach is already beginning to show up in project backlogs. For example, Kinder Morgan reports a roughly $10 billion backlog with about 60% linked to power demand, while TC Energy is advancing smaller, high-return expansions specifically sized for regional power-load growth. These trends suggest the model will begin to show up in earnings even more clearly in the second half of the decade.

4. Capital allocation is expected to tilt further toward brownfield expansion and asset sweating.

New build combined cycle capital costs have already risen to $2,500–$3,000+ per kW, with projections approaching $4,000 per kW for projects completed near 2031. As these projects scale, execution risk is increasingly shifting toward the supply chain, with compressor and engine OEMs, EPC firms, and power-focused developers facing tighter schedules, longer equipment lead times, and more complex coordination across gas, power, and grid interfaces. As a result of these persistent EPC bottlenecks and supply chain pressures, higher utilization of the existing CCGT fleet, pipeline looping, compression, and storage expansion are likely to dominate near-term capital deployment.

5. Natural gas is set to remain the system’s reliability backbone through the end of the decade.

Even with continued growth in renewables and batteries, dispatchable gas generation is expected to carry the marginal reliability function as load volatility rises. Recent instances of power prices approaching $250/MWh and spark spreads exceeding $200/MWh illustrate the value of firm gas supply and reinforce the incentive to contract for reliability rather than rely on spot markets.

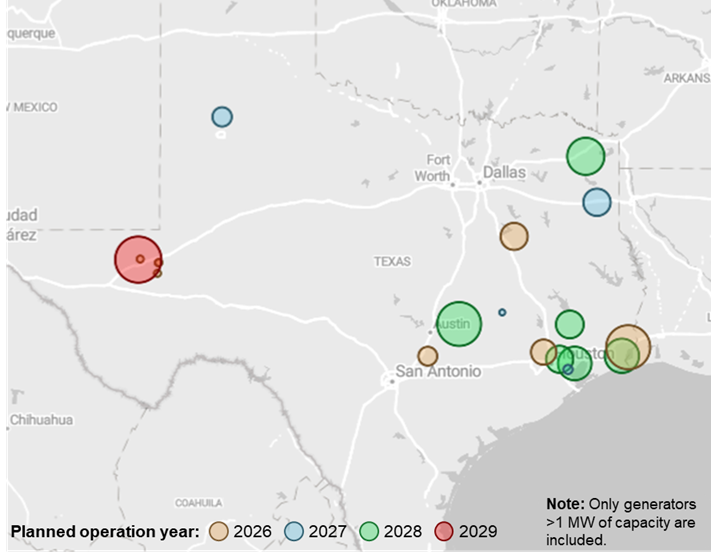

Exhibit 2: Planned natural gas-fired power additions in Texas. (Source: EIA, ADI Analytics)

6. Storage and peak‑shaving assets are expected to move closer to the load.

Storage strategy is shifting from seasonal optimization toward operational resilience. High‑deliverability storage and flexible pipeline contracts are increasingly positioned to support short‑duration demand spikes, weather stress, and data‑center‑specific reliability requirements. This trend favors assets located near major load pockets rather than basin‑centric storage.

7. Fuel flexibility is likely to determine long‑term optionality rather than near‑term volumes.

Over the remainder of the decade, infrastructure is expected to be engineered with optionality for RNG, ammonia, or hydrogen, even as natural gas remains the primary fuel. Turbine manufacturers are targeting 100% hydrogen‑capable designs by around 2030, but limits on hydrogen production, transport, and cost suggest adoption will trail equipment readiness. The near‑term value lies in preserving future compliance paths rather than displacing gas burn.

8. Policy and regulation are likely to favor contracted, regulated growth over merchant exposure.

Federal permitting momentum is shortening timelines for pipeline and related infrastructure, while state‑level outcomes continue to diverge. At the same time, affordability concerns are pushing regulators to require greater cost sharing from large industrial and data‑center customers. This environment favors contracted, regulated earnings and reinforces investor preference for de‑risked organic growth over transformative M&A.

The bottom line

Over the next five years, midstream companies are expected to shift further toward integrated power‑linked platforms, with growth driven by AI‑related load, constrained grids, and a rising premium on reliability. Cashflow visibility will increasingly depend on executing brownfield expansions, securing long‑term contracts tied to large loads, and preserving fuel flexibility as policy and technology evolve.

These themes sit at the center of the Gas‑to‑Grid Infrastructure Conference, which brings together pipeline operators, power developers, utilities, data‑center operators, and policymakers to examine how gas supply, generation, storage, and grid delivery are being aligned for the next phase of load growth.

– Uday Turaga & Piercen Hoekstra

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.