ADI Analytics hosted its first North America Natural Gas and NGL Forum in Houston late February. The forum was well-attended with representatives from a wide range of companies including integrated oil and gas majors, refiners, E&P independents, industrial gas suppliers, equipment providers, technology licensors, investors, and media outlets.

The forum featured several presentations by ADI analysts and panel sessions, featuring external speakers and industry experts. The presentations highlighted key demand drivers, supply outlook, pricing forecasts, strategic implications, investment opportunities, and regulatory concerns around natural gas and NGLs. The panel sessions built off of the presentations and featured in-depth discussions focusing on small- and mid-scale LNG, natural gas conversion to fuels, and new innovations including the Industrial Internet of Things.

In our presentation we gave an outlook for NGL supply, demand, and pricing through 2020 and focused on key topics impacting the NGL market. This include addressing where the supply is coming from, how much demand will grow, how ethane supply in the Gulf Coast will be impacted, and will new LPG export terminals are expected?

NGLs have many end uses

NGLs are produced along with natural gas or crude oil and have many end uses. For instance, ethane (C2) is used for power generation and as a petrochemical feedstock for ethylene production. Propane (C3) is used as a cooking fuel and has applications as a petrochemical feedstock. Butane (C4) can be used as a refinery feedstock and can be blended with propane (LPG) or pentane. Lastly, pentane (C5+) is widely used in gasoline as a fuel for transportation.

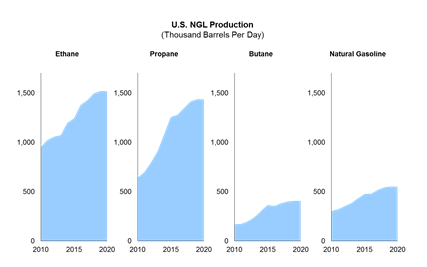

NGL production growth is slowing

Due to the shale boom in the U.S. which produced large volumes of crude oil and natural gas, NGL production grew significantly. NGL production in the U.S. grew from 2,100 thousand barrels per day (mbpd) in 2010 to 3,300 mbpd in 2015. NGL production in the U.S. is expected to continue to increase through 2020, but at a much slower rate than it did in the previous five years.

Given current drilling rates and our assumption of oil prices being $50 – $70 per barrel through 2020, we expect NGL production to increase moderately to ~3,900 mbpd by 2020. Ethane and propane production are expected to reach 1,500 mbpd each by 2020, while butane and pentane will be closer to 500 mbpd over that period. Figure 1 breaks down NGL production by component.

Most of the production is coming from the Eagle Ford, Permian, Anadarko, and the Marcellus plays. Production growth will primarily come from the Permian while the Utica is expected to experience a slight decline which will be offset by production growth nearby in the Marcellus.

Exhibit 1: U.S. NGL Production by Components

(Source: EIA)

Ethane demand surpasses supply

Historically, ethane demand has been dominated by ethylene crackers but ethane exports began in 2016 as the first ethane shipments from Sunoco’s Marcus Hook and Enterprise’s Morgan’s Point terminal both departed to petrochemical plants in Europe and Asia. In addition to the two ethane terminals, a number of ethylene crackers are under construction and are expected to start consuming ethane starting in 2017 and 2018. Collectively, ethane demand will rise significantly and will likely be difficult to meet with projected supply likely driving up ethane prices.

New LPG terminals reduce Gulf Coast supply

LPG export terminals have been the primary driver for propane and butane demand and more are coming on-stream soon. New export terminals on the East Coast will increase exports of local NGL production potentially reducing pipeline transfer volumes to the Gulf Coast. Marcus Hook will increase LPG exports by 350 mbpd along the East Coast, reducing supply volumes into the Gulf Coast. In addition to LPG exports, small volumes of propane demand will come from new propane dehydrogenation units accounting for an additional 113 mbpd by the end of 2017. Due to the increase in propane demand, we expect prices to steadily increase by 2020.

The NGL market presents great risks and opportunities

There are a number of factors impacting the demand outlook for NGLs as they play a critical role in a variety of markets. This includes U.S. cracker feedstocks, LPG fuel use in emerging markets, U.S. fuel blending, and cracker feedstock choices. For instance, a decline in Asian LPG prices can cause U.S. exports to fall sharply while an uptick in emerging economies’ GDP will increase LPG demand.

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.