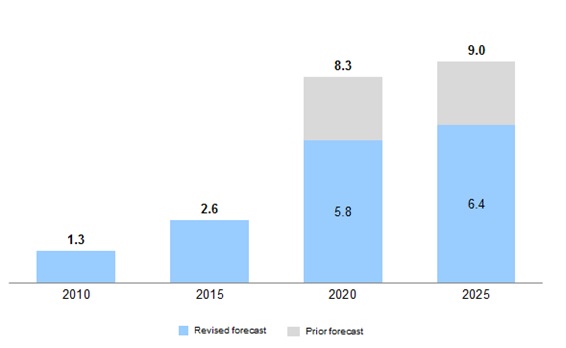

In 2014, China’s LNG demand peaked at 2.7 billion cubic feet per day (bcfd) making it the third-largest LNG importer in the world behind Japan and South Korea. However, as the Chinese economy has slowed LNG demand declined for the first time since China started importing LNG in 2006. Exhibit 1 highlights the revised LNG demand forecast for China. This decline has led to a slowdown in construction of new regasification terminals and growing uncertainty around the outlook for small-scale LNG.

Delays in terminal construction

Currently, China has 13 LNG import terminals in operation with a cumulative capacity of 5.4 bcfd and had planned to construct several more through 2019 which would add an additional capacity 3.4 bcfd. Due to the slowing and uncertain outlook for LNG demand, startup for several of these projects has been delayed. Many of the contracts to supply LNG to the new regasification terminals were signed when oil prices were above $100 per barrel. Now that oil is at less than $50 per barrel, both spot LNG and LPG (liquefied petroleum gas) prices are more competitive. Oil and gas companies have been actively trying to suspend shipments of contracted LNG to the new terminals and instead buy lower-priced spot LNG. LPG is also being preferred by the terminal’s customers as it is cheaper than LNG priced under longer-term contracts.

Exhibit 1: Prior and revised Chinese LNG demand forecast (billion cubic feet per day)

Small-scale LNG may slow down

Since 2013, China has been investing heavily in LNG in an effort to improve air quality and restructure their domestic energy market. Their plan is to first introduce LNG as a marine fuel on inland waterways, then for coastal vessels, and finally for deep sea-going ships. So far, they have begun developing a market for LNG as a marine fuel and have created three small-scale LNG carriers. Over the next five years, China is hoping to increase the number of inland vessels which use LNG as a fuel from 2% to 20%.

However, there are a few challenges in implementing LNG fueled ships in China. For example, the economic benefits are uncertain, LNG fueled ships are more complex than diesel fuel systems, and there has been limited progress on establishing an LNG bunkering infrastructure in China. LNG-fueled vessels cost ~20% more to build than equivalent diesel ships and can accommodate less cargo. In addition to cost, there is a lack of manufacturing expertise as China has been heavily reliant on foreign companies in these areas in the past. Also, it will be challenging to implement LNG-fueled ships in China because of the lack of subsidies for ship owners to invest in bunkering development. In an effort to increase adoption, emission standards are being developed for ship engines and subsidies are being offered to Chinese ship operators to build LNG-fueled ships.

-Brandon Johnson and Uday Turaga

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.