Russia has historically been a major player in the global oil market, not only as a leading crude oil exporter but also as a significant supplier of refined oil products. For years, it has been a key source of diesel, fuel oil, and other refined oil products for Europe, Asia-Pacific (APAC) including China, and CIS countries. However, the dynamics of the refining market have shifted considerably since the start of the Russia-Ukraine war in late February 2022.

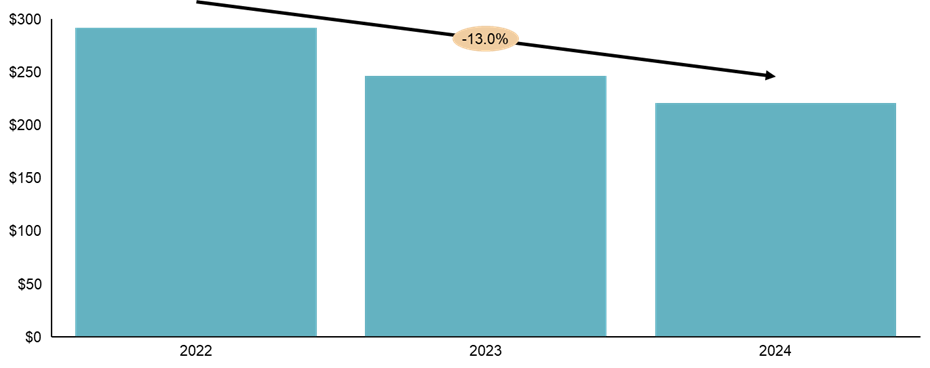

In 2023, ADI Analytics published a blog about the impact of the war and Western sanctions on the Russian fossil fuel market. For instance, the G7 price cap on Russian oil and refined oil products, along with restrictions on shipping and insurance services, has led to discounted prices and a massive shift toward export markets in South America and Asia, such as Brazil, Turkey, China, and India. Although Russia has managed to find new buyers for its refined oil products, economic sanctions continue to hurt Russian refiners. Russia’s export revenue for refined oil products has slumped by 13% annually, reaching an average of ~$220 million per day in 2024—a noticeable drop since 2022 levels (see Exhibit 1).

Exhibit 1: Russia’s refined oil products export revenue (USD million per day) (Source: Centre for Research on Energy and Clean Air, ADI Analytics)

As of the time this blog is being posted, the U.S. and Russia are engaged in ceasefire negotiations, though no agreement has been reached. Should the peace talks come to fruition, several key implications for the global refining market could emerge:

The rest of this article is available to ADI Plus subscribers.

Log in or subscribe to unlock ADI Plus content >>

Have questions? We're happy to help.

About ADI Analytics

ADI is a prestigious, boutique consulting firm specializing in oil and gas, energy, and chemicals since 2009. We bring deep expertise in a broad range of markets where we support Fortune 500, mid-sized and early-stage companies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum that brings c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum.

Subscribe to our newsletter or contact us to learn more.