The U.S. SAF industry has faced significant uncertainty recently, with questions surrounding how government support, feedstock eligibility, and financial incentives might evolve during President Trump’s second administration. Our recent blog, “The Future of SAF Under Trump: Will Biofuels Thrive or Stall?” highlighted these concerns and emphasized the potential impacts on SAF investments and production strategies. The recent release of the 45Z Clean Fuel Production Credit (CFPC) guidance on January 10, 2025, offers some clarity but also kicks the can down the road on several issues and sets the stage for shifts in investment priorities and production approaches across the SAF industry.

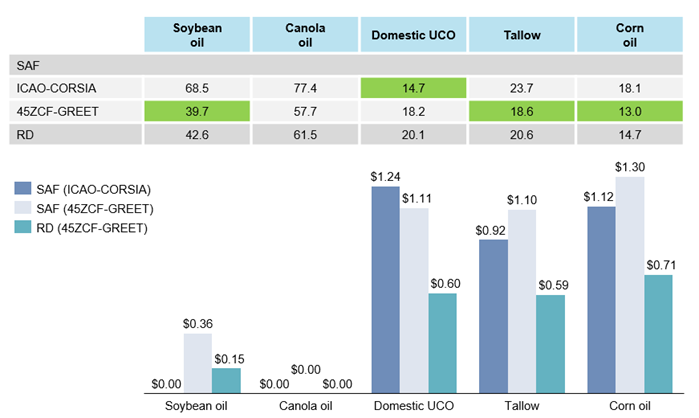

Exhibit 1: Default CI values (kg CO2e per MMBtu) for 45Z and estimated credits ($/gallon).

As shown in Exhibit 1, the updated 45ZCF-GREET model introduces key changes that apply to both SAF and non-SAF producers, allowing them to choose between the ICAO-CORSIA and 45ZCF-GREET models to optimize CI scores and financial benefits. The revised 45ZCF-GREET model favors feedstocks such as soybean oil, tallow, and corn oil for SAF production, while domestic used cooking oil (UCO) has a better CI score under the ICAO-CORSIA model. However, canola oil remains ineligible for incentives under both models. Additionally, the updated 45ZCF-GREET model does not include climate-smart agriculture (CSA) practices or carbon capture and storage (CCS) considerations, which makes it more difficult for corn ethanol to meet the 50% decarbonization threshold necessary for SAF credits.

In addition, some of the key elements of the recently released 45Z guidance include the follows:

1. Imported UCO is now ineligible for the credit through the GREET model. Excluding imported UCO will increase the reliance on more expensive domestic feedstock alternatives like UCO, soybean oil, and tallow. This shift could hinder the scalability of SAF production in the U.S. and reduce the competitiveness of U.S. SAF in the global market.

2. Coverage of fuels has expanded beyond motor and aviation to include marine fuels. The scope of expanding SAF coverage to include marine fuels will likely intensify competition for limited bio-feedstocks and drive up prices, leading SAF producers to struggle to secure affordable and sufficient supplies.

3. The new 45Z guidance requires “substantial processing” to qualify for the credit. This excludes blending fuel mixtures, intermediate sales (e.g., sale of ethanol to alcohol-to-jet facilities), compression of renewable natural gas (RNG) streams without processing to remove impurities, and imported finished fuels that need only “minimal processing.” The per-facility Inflation Reduction Act (IRA) credit limits under the new 45Z guidance may realign investment strategies, where refiners will carefully assess which credit—SAF (45Z), hydrogen (45V), or CCS (45Q)—offers the best return, which shapes future production priorities.

4. The provisional 45Z guidance reiterates anti-stacking with a limit of one IRA credit (45Z, 45V, 45Q, or 45Y) per facility.

5. Finally, the guidance requires producers to certify production processes using accredited verifiers, such as individuals or organizations from International Sustainability and Carbon Certification (ISCC), Roundtable on Sustainable Biomaterials (RSB), and International Civil Aviation Organization (ICAO).

Consequently, these updates will likely shift producers’ feedstock preferences, where they opt for feedstocks with the most favorable CI scores to maximize returns. However, regulatory uncertainties persist as the U.S. Department of the Treasury has yet to finalize the tracking and verification rules for imported UCO, which remains ineligible for 45Z credits until those rules are established. Besides, the lack of detailed guidance on CSA practices in the 45ZCF-GREET model could hinder broader SAF adoption. Meanwhile, the U.S. Department of Agriculture (USDA) released an interim rule for CSA in biofuel feedstocks, which Treasury may use in the final 45Z guidance, including a feedstock CI calculator.

Looking ahead, the future of the U.S. SAF industry will highly depend on the finalized 45Z guidance following a 90-day comment period. With pending decisions surrounding the post-2027 fate of 45Z credits and potential modifications to IRA incentives under the Trump Administration, long-term strategic planning and investment decisions remain complex and uncertain.

– Christine Ho and Panuswee Dwivedi

ADI Analytics is a prestigious, boutique consulting firm specializing in oil & gas, energy transition, and chemicals since 2009. We bring deep, first-rate expertise in a broad range of markets including up-to-date sustainable aviation fuels (SAF) policy insights, regulatory compliance, and market dynamics, where we support Fortune 500, mid-sized and early-stage companies, government agencies, and investors with consulting services, research reports, and data and analytics, with the goal of delivering actionable outcomes to help our clients achieve tangible results.

We also host the ADI Forum, one of Houston’s distinguished industry conferences, to bring c-suite executives together for meaningful dialogue and strategic insights across the oil & gas, energy transition, and chemicals value chains. Learn more about the ADI Forum, which is chaired by Uday Turaga, Founder & CEO, ADI Analytics, at www.adi-forum.com.

Subscribe to our newsletter or contact us to learn more.