The shale gas boom in North America has drawn a lot of attention to LNG exporting projects in the United States, but there are several projects based in Canada that are also aiming to export the regional surplus of natural gas. These projects have the same aim as the projects in the United States but there are three important differences that make their story unique.

First, the Canadian LNG projects are aiming to export mainly to Asian markets. There have been nine projects that have received National Energy Board (NEB) export approval. The National Energy Board is the Canadian Equivalent of the U.S. Department of Energy. The regulatory process in Canada is similar to the process in the United States. Each project must receive environmental, export and construction approval. The largest difference is that there is not a distinction between FTA and non-FTA export approval. Once a project receives export approval they are able to export to any country that Canada has a trading relationship with.

Total planned output for the Canadian projects, which have received export approval from the NEB, is ~135 mtpa. The majority of that output is provided by four projects which total 99 mpta. The projects, LNG Canada, Prince Rupert LNG, Aurora LNG and West Coast Canada LNG, are planned to have capacities of 24, 21, 24 and 30 mtpa, respectively. LNG Canada is being promoted by Shell, PetroChina, KOGAS and Mitsubishi. Prince Rupert is being developed by the BG Group. Aurora LNG is led by Nexen Energy, INPEX, and JGC. Finally, West Coast Canada is owned by ExxonMobil and Imperial Oil.

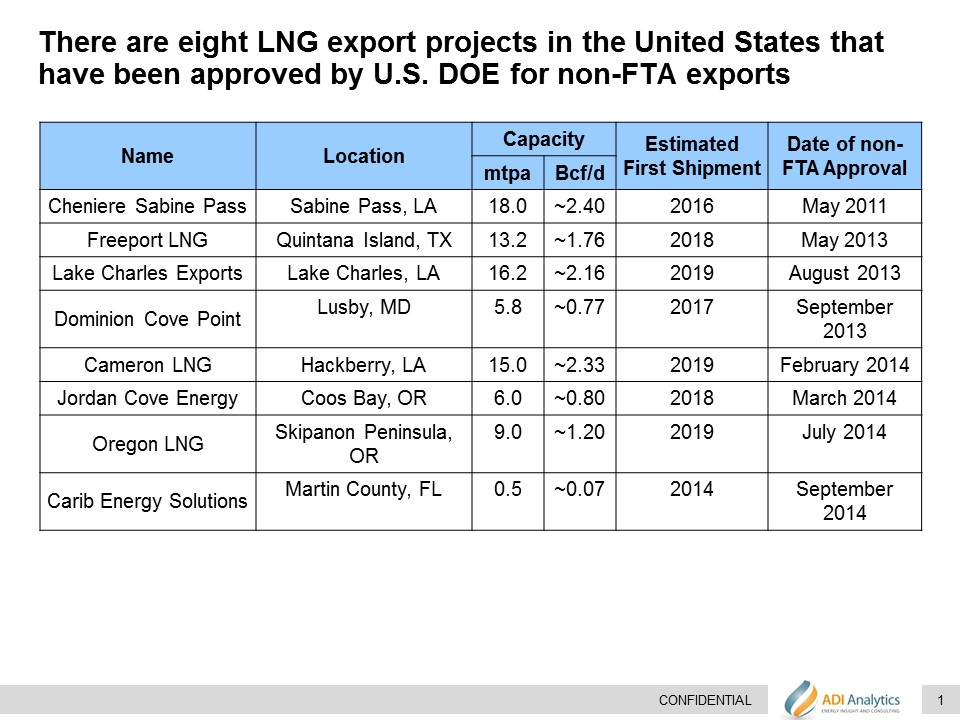

Non-FTA Approved U.S. Projects

NEB Approved Projects

Second, the timeline for these projects in relation to their U.S. counterparts is further out. Cheniere’s Sabine Pass terminal is scheduled to be in service during 2016 and will be the first in several American export projects to be commissioned. In comparison, the first major LNG export project in Canada is estimated to come online in 2017 or beyond. This delay can be directly linked to the location of the Canadian projects. Most of the locations, in addition to construction of the liquefaction trains, also require the construction of pipelines, hundreds of miles long, in order to supply feed gas.

Finally, Canadian projects also have higher costs associated with producing LNG due to the fact that most construction is happening on greenfield sites instead of brownfield sites like their U.S. counterparts. Further, several of these project locations have difficult conditions for constructing capital projects. Finally, most of the locations, in addition to construction of the liquefaction trains, also require the construction of pipelines, hundreds of miles long, in order to supply feed gas from the natural gas fields in Canada. Collectively, these raise project capital costs, which average at over $1000 per ton for most projects in comparison to costs around $700-$800 for many U.S. projects

Given these challenges, which will be further exaggerated by the falling price of oil, project developers have been having second thoughts. For example, one of the major projects, Kitimat LNG, lost one of its key stakeholders, Apache, a few months ago. The Australian LNG player, Woodside, recently stepped in and acquired Apache’s interest in Kitimat LNG. Moving forward, with all of the issues in mind, it may be difficult for Canadian LNG exporters to compete with exports from the United States

-Tyler Wilson and Uday Turaga